Hormuz Chokes Again — and the VLCC Market Must Reprice Risk

Renewed attacks have disrupted the recovery in Gulf shipping, restricting effective tanker capacity and forcing charterers, owners and Chinese refiners to reassess their August exposure

The Strait of Hormuz may remain physically navigable, but for many commercial operators it is again approaching a functional closure.

A series of attacks in early July has sharply reversed the gradual recovery in shipping traffic through the waterway. Merchant ships have been hit, vessels have turned back from the Gulf, and owners are once again weighing the commercial value of a voyage against the safety of their crews and assets.

Under normal conditions, an estimated 125 to 140 vessels pass through Hormuz each day. In the immediate aftermath of the latest escalation, daily traffic reportedly fell to between 20 and 30 ships. Some vessels continued to transit with their AIS signals switched off, further reducing transparency around actual movements.

The consequences extend well beyond a temporary interruption to Gulf exports. The renewed security crisis has overturned assumptions about available VLCC capacity, complicated the reopening of LNG supply chains and added another layer of uncertainty to China’s crude-import and inventory strategy.

August VLCC assumptions no longer hold

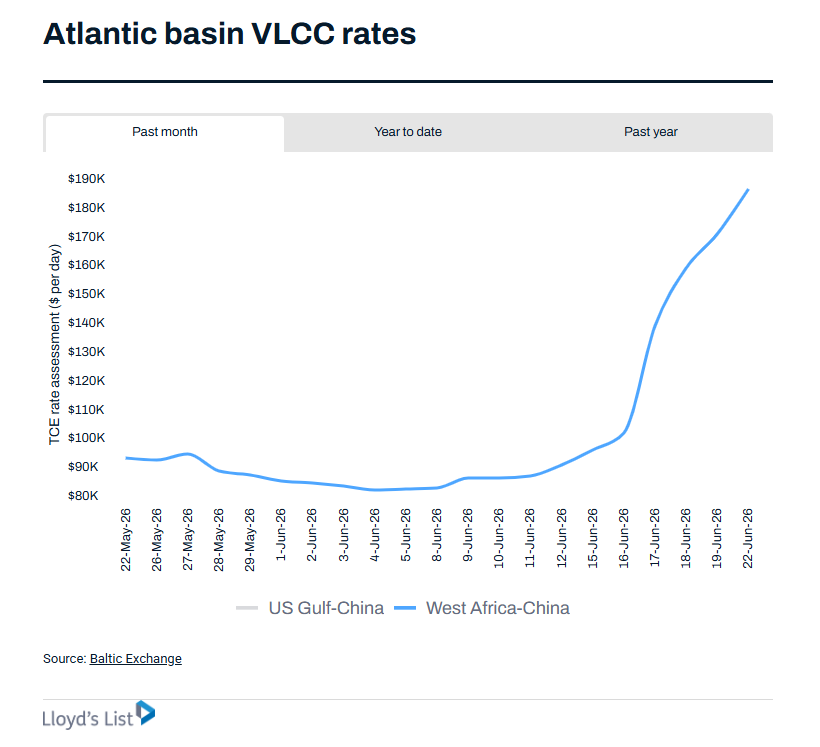

Only days before the latest attacks, the VLCC market appeared to be moving towards a more difficult August.

Tankers that had been trapped or delayed inside the Gulf were gradually returning to the wider market. Ships that had previously taken longer diversion routes were expected to re-enter shorter trading patterns. At the same time, China’s crude restocking remained cautious, limiting immediate cargo demand.

That combination pointed towards rising vessel availability and softer earnings.

The renewed deterioration in Hormuz has interrupted that process.

Ships expected to leave the Gulf are again hesitating. Vessels positioned outside the strait are reluctant to enter. Tankers that might otherwise have returned to shorter routes could remain tied up in longer voyages or waiting patterns.

This is creating a renewed gap between nominal fleet supply and commercially available capacity.

A VLCC may appear available in fleet statistics, but it offers little immediate supply if its owner will not accept a Gulf voyage, its insurer imposes prohibitive conditions, or its crew cannot be guaranteed a safe transit.

Should traffic through the strait remain below roughly 50 ships per day for several more weeks, VLCC rates could return to a pattern of sudden and volatile increases. Each vessel willing and able to perform a Middle East voyage would carry a significant security premium.

War-risk insurance costs are also rising again, with additional premiums for a single Gulf transit potentially reaching hundreds of thousands of dollars. Those costs will ultimately flow into freight negotiations.

The market is therefore repricing fear, availability and execution risk. Such increases can be powerful, but they are also less stable than freight strength generated by sustained cargo growth.

LNG shipping faces the greatest operational sensitivity

LNG carriers are among the vessels most exposed to the latest escalation.

Several Qatar-linked LNG carriers reportedly turned away while heading towards Ras Laffan after the attacks. More than ten ballast LNG vessels were said to be waiting outside the port, while dozens of Qatar- and UAE-controlled ships remained positioned across the Gulf, India and the Malacca region.

The safety threshold for LNG operations is particularly high. A serious incident involving an LNG carrier could have consequences far beyond the loss of a conventional cargo vessel. Owners therefore require a high degree of confidence in naval protection, port access, insurance coverage and emergency response arrangements before committing tonnage.

This creates a difficult stand-off. Exporters need ships to resume loadings, while owners need credible security assurances before sending vessels into the Gulf.

Oil tanker movements present a more mixed picture.

Some VLCCs that had been delayed for months managed to leave during a brief easing in tensions. Yet outbound vessels may be unwilling to return, while incoming ballast ships are turning away or waiting outside the Gulf.

The result is an uneven release of trapped tonnage without a reliable inflow of replacement capacity.

Accurate fleet accounting has also become increasingly difficult. Large numbers of ships are operating without visible AIS signals, limiting the ability of charterers, brokers and intelligence providers to assess congestion and available supply.

The human consequences remain substantial. Thousands of seafarers are reportedly still aboard vessels waiting within the Gulf, with owners and crews unable to predict when normal operations will resume.

Higher costs for China’s crude supply chain

China, as the world’s largest crude importer, is highly exposed to any prolonged disruption in Hormuz.

Chinese refiners entered the second half of the year facing a difficult inventory decision. Crude imports had weakened significantly during the first half, suggesting that some degree of restocking would eventually be required. The timing of that restocking now coincides with renewed security pressure in the Gulf.

If VLCC rates rise again, freight costs from the Middle East to China will increase alongside insurance and operational expenses. Refiners must then decide whether to secure cargoes and tonnage at elevated prices or wait for a possible easing in both oil and freight markets.

Waiting carries its own risks. A prolonged disruption could leave refiners competing for a smaller pool of acceptable vessels precisely when restocking demand begins to strengthen.

The pressure could also spread into refined-product markets.

Global diesel supply has tightened amid refinery disruptions, export restrictions and stronger European margins. Chinese refiners may find improved opportunities in export markets, although higher exports must be balanced against domestic supply requirements.

That tension between export profitability and domestic stability could become more difficult to manage if crude procurement costs rise sharply.

Chinese shipowners face a larger risk premium

Chinese and other Asian tanker owners active in Middle East trades must also reassess voyage economics.

Every Gulf fixture now requires closer examination of insurance exclusions, crew safety, charter-party clauses, deviation rights and responsibility for additional war-risk premiums.

Operating with AIS switched off may reduce visibility, but it introduces additional navigational, compliance and insurance complications. In the event of a casualty, disputed AIS practices could significantly complicate claims and liability assessments.

Owners will therefore seek clearer contractual protection before accepting Gulf employment. Charterers may have to pay more for vessels with suitable insurance, experienced crews and an established record of operating in high-risk waters.

The premium will increasingly reflect operational certainty rather than vessel supply alone.

A strategic warning for China

The crisis also highlights a broader structural issue.

China is a leading crude importer, the world’s dominant shipbuilding nation and an increasingly important owner of large tanker fleets. Each disruption to global energy trade reinforces China’s position across the maritime supply chain.

At the same time, greater participation creates greater exposure.

A significant share of China’s imported energy still depends on a narrow maritime gateway. When access to that gateway becomes uncertain, freight costs, insurance pricing, refinery planning and national energy security are affected simultaneously.

The current disruption strengthens the case for more diversified crude sourcing, stronger marine insurance capabilities, greater control over strategic shipping capacity and deeper contingency planning for alternative logistics arrangements.

Hormuz remains open on the map. Commercially, however, its capacity is being determined by missiles, insurance underwriters, naval protection and the willingness of seafarers to sail.

For the VLCC market, that means August can no longer be assessed through conventional vessel-supply calculations alone.

The decisive variable is now the number of ships that can enter, load and leave the Gulf with an acceptable level of risk. Until that number recovers, effective tanker capacity will remain constrained, freight rates will remain vulnerable to sudden spikes, and the cost of China’s next crude-restocking cycle will be increasingly difficult to predict.

READ MORE

Tankers

Tankers

Exclusive Interview | Trafigura’s Andrea Olivi: Ships and Ports Are Becoming Strategic Assets

Tankers

Tankers

Fratelli Cosulich Takes Delivery of Second Methanol-Ready Bunker Tanker

Tankers

Tankers

20-Year-Old VLCC Fetches $50M – Market Logic Turned Upside Down

Tankers

Tankers

Shenghang plants flag in Singapore as Chinese chemical tanker owner goes global

Tankers

Tankers

First Ammonia-Fuelled Ship Loads Green Ammonia in China

Tankers

Tankers