An 18-Year-Old VLCC Just Made $32m in a Year

A nearly 18-year-old VLCC has delivered a remarkable asset play, after shipbroking house SSY reported that the 314,000-dwt LILA KOCHI has been sold to Mediterranean Shipping Co for $79m.

The Kawasaki Heavy Industries-built tanker, delivered in Japan in 2008 and fitted with a scrubber, was reported sold to MSC in a deal that was only recently disclosed to the market. However, shipbroking sources said the transaction was actually concluded several weeks earlier.

The price marks a striking increase from the vessel’s previous transaction. The ship, formerly known as M. STAR, was reported sold by MOL in May 2025 for around $46.7m to $47m, with GMS understood to be the buyer at the time.

Based on that earlier acquisition price, the latest $79m resale would imply a gross paper gain of about $32m for GMS, equivalent to an uplift of close to 70% in just over a year, before transaction costs and any capital expenditure.

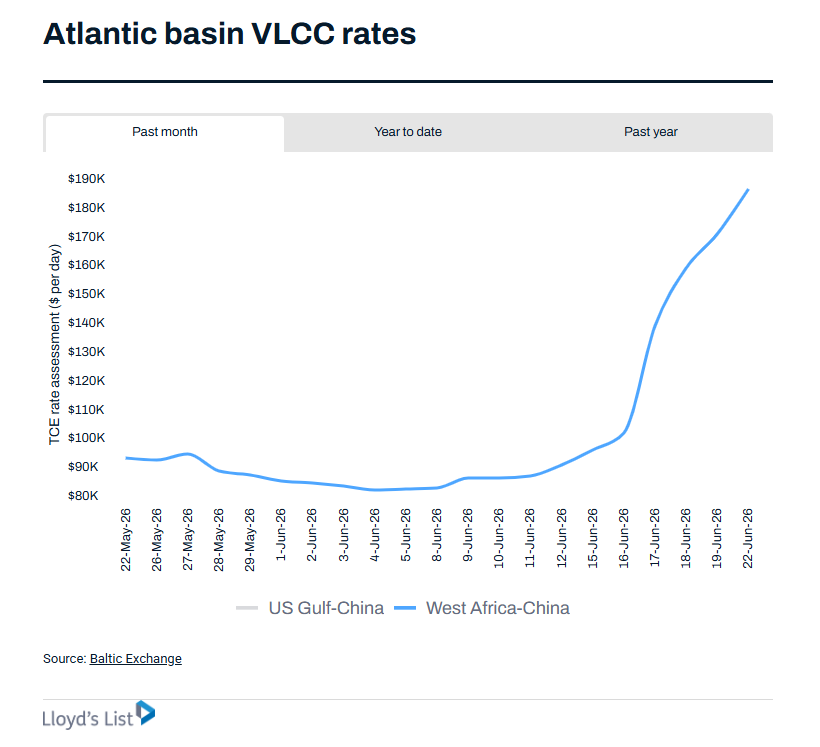

For an 18-year-old VLCC, the number is exceptional. The sale price is not merely a reflection of steel, age and depreciation, but of a secondhand tanker market where available VLCC tonnage has become increasingly scarce and strategic buyers are prepared to pay up for immediate exposure.

Several factors likely supported the valuation. LILA KOCHI is a Japanese-built VLCC from a top-tier yard, comes with scrubber economics, and sits in a segment where older but well-built large crude carriers have attracted strong interest amid firm tanker earnings and limited prompt supply.

The buyer’s identity is also important. MSC has emerged as one of the most closely watched names in the recent VLCC sale-and-purchase market, alongside the wider Sinokor-linked buying wave that has absorbed a significant number of large crude tankers over the past several months.

The transaction underlines how far VLCC asset values have moved. A vessel that changed hands for less than $50m last year has now been priced close to $80m, despite being one year older. That suggests the current market is being driven less by traditional depreciation models and more by scarcity, earnings expectations and the strategic value of controlling large tanker capacity.

For GMS, the deal stands out as one of the clearest examples of the asset-price surge in the VLCC market. For MSC, it is another signal that the group is continuing to build exposure to large tanker tonnage at a time when control of available VLCC supply is becoming a market theme in its own right.

READ MORE

Tankers

Tankers

The Second Surge: How Geopolitics and the Strait of Hormuz are Rewriting VLCC Freight Rates

Tankers

Tankers

Nearly 400 VLCCs Have Been “Controlled”

Tankers

Tankers

Angelicoussis Group’s Marina: Hormuz Crisis Is Redrawing Global LNG Trade Flows

Tankers

Tankers

WS 897! A Single VLCC Voyage Could Earn $30 Million: How Sinokor Capitalized on Persian Gulf Risks for an Astronomical Premium

Tankers

Tankers