The Second Surge: How Geopolitics and the Strait of Hormuz are Rewriting VLCC Freight Rates

Recently, the global Very Large Crude Carrier (VLCC) market has experienced its second massive freight rate surge since the outbreak of geopolitical conflicts. Although actual crude oil flows through the Strait of Hormuz remain at very low levels compared to pre-crisis times, the shipping market's expectations of the strait's imminent reopening have already triggered a restructuring of global capacity distribution.

Global Freight Rate Surge

According to Baltic Exchange data, spot freight rate indicators on multiple key routes have recorded staggering increases.

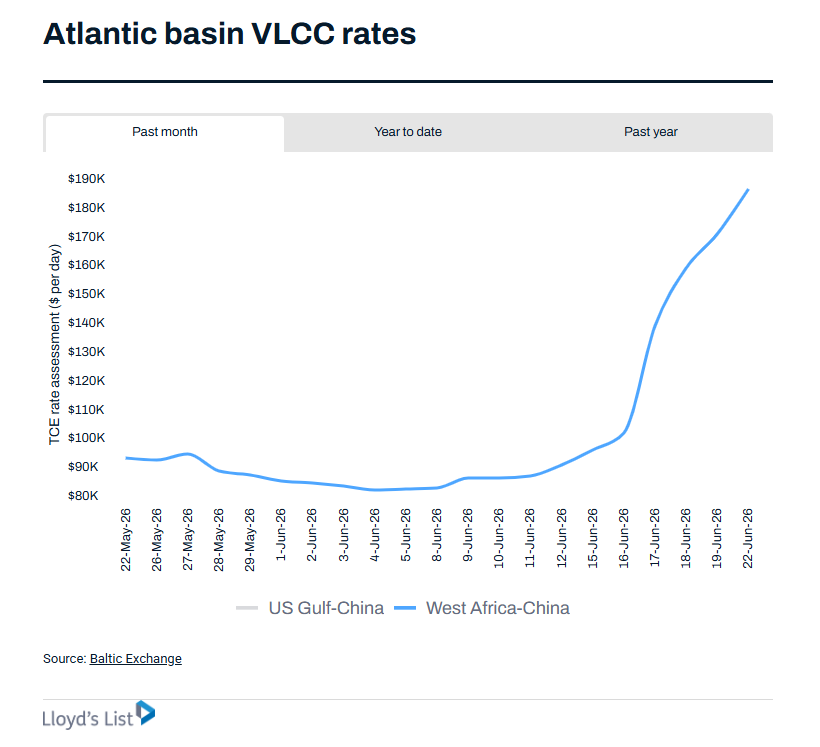

Taking the Atlantic basin as an example, the daily Time Charter Equivalent (TCE) rate for VLCCs on the West Africa-to-China route soared to $188,957 per day, a massive 92% week-on-week jump, hitting its highest level since early March. Similarly, daily rates for the US Gulf-to-China route climbed to $154,987 per day, up 46% week-on-week.

Furthermore, the Oman-to-China route index, which assesses loading volumes outside the strait, surged 82% in a single week to reach 276 points on the Worldscale (WS), equating to daily earnings of $275,032—an all-time high since the introduction of this index. Meanwhile, the theoretical assessment price for the Middle East Gulf-to-China route, which evaluates loading inside the strait, remained at an extremely high level of $412,888 per day.

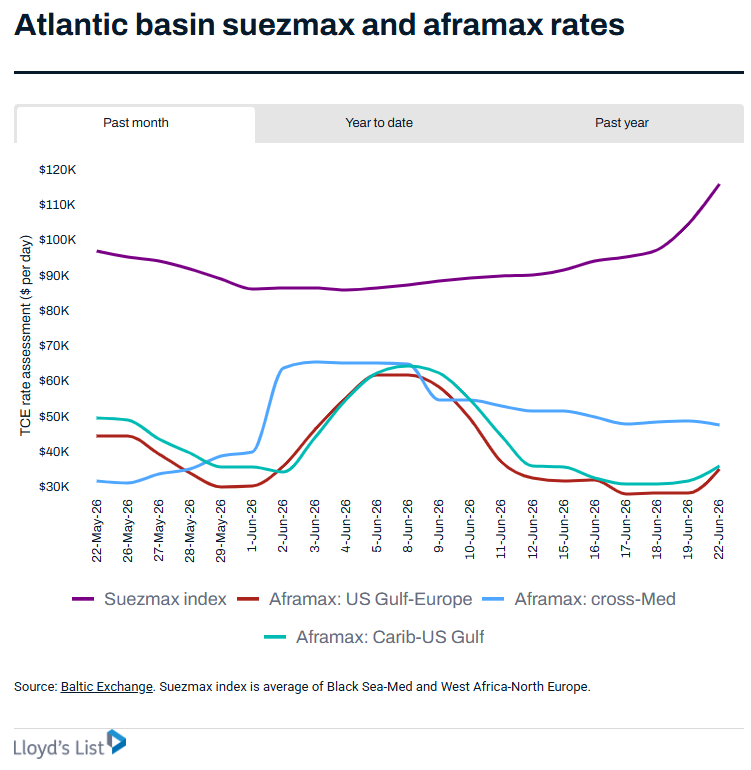

In stark contrast, rates for medium-range (MR) product tankers in the Atlantic basin plummeted due to weak demand, reflecting the unique position of crude tankers in this crisis.

Reasons for the Freight Rate Surge

The core driving force behind this crude tanker freight rate surge is not a recovery in actual trading volumes, but rather strong expectations of reopening and the subsequent inefficiencies in fleet operations.

I. Magnetic Effect and Global Capacity Imbalance

First, the hope of the strait's potential reopening has created a massive "magnetic effect," leading to a severe imbalance in global capacity distribution. Ship tracking data indicates that a large number of empty VLCCs, having discharged their cargo in Asia, are exiting the Strait of Malacca and abandoning their regular routes to the Atlantic basin, turning north toward the Middle East instead. Currently, about 60 empty tankers have gathered off the coast of Oman, waiting for permission to pass through the Strait of Hormuz, with more than 75 additional tankers heading to those waters. This pursuit of potentially high-yield cargoes in the Middle East has directly drained effective capacity from the Atlantic and other key loading ports, causing localized capacity shortages worldwide and systematically driving up spot market quotes.

II. Fuel Costs Reshape Economic Decisions

Second, persistently high fuel costs have fundamentally altered shipowners' economic decision-making models. Global marine fuel prices are currently still about 50% higher than pre-crisis levels. Under such exorbitant operating costs, the economic appeal of long-haul empty voyages westward to the Atlantic basin has significantly diminished. Shipowners prefer to wait for opportunities in the closer Middle East region, further reducing the availability of vessels allocated to the Western Hemisphere.

Future Outlook

Looking ahead, constrained by the prolonged nature of geopolitical maneuvering and reshaped risk perceptions, freight rates for Middle Eastern and global crude tankers are expected to continue receiving strong support.

In the short term, if the strait's reopening process is further delayed or if transit conditions remain chaotic and stop-and-go, the number of idle tankers waiting outside the strait will continue to swell. Available capacity in regions like West Africa is already experiencing severe shortages. Anticipating further rate increases, many shipowners have adopted a wait-and-see strategy, withholding capacity and temporarily refusing orders, which will push Atlantic basin and global spot freight rates to continue their upward climb in the near term.

In the medium to long term, the industry generally believes that the geopolitical risk premium has become semi-permanent. Given that Middle Eastern waters have proven vulnerable to blockades, the market's risk assessment models have fundamentally changed. Even if the strait fully resumes normal commercial transit in the future, the war risk insurance premium for a single transit remains close to 1% of the hull value (approximately $2 million), which is significantly higher than the pre-crisis rate of 0.1%. This increase in costs and the lingering shadow of blockades mean that loading routes in the Middle East will continue to carry a high geopolitical premium for months or even years to come, setting a higher floor for global freight rates.

READ MORE

Tankers

Tankers

An 18-Year-Old VLCC Just Made $32m in a Year

Tankers

Tankers

Nearly 400 VLCCs Have Been “Controlled”

Tankers

Tankers

Angelicoussis Group’s Marina: Hormuz Crisis Is Redrawing Global LNG Trade Flows

Tankers

Tankers

WS 897! A Single VLCC Voyage Could Earn $30 Million: How Sinokor Capitalized on Persian Gulf Risks for an Astronomical Premium

Tankers

Tankers