Exclusive Interview | Trafigura’s Andrea Olivi: Ships and Ports Are Becoming Strategic Assets

From fewer than 100 vessels to around 500: how Trafigura is redefining shipping capability for global commodity trading By Xinde Marine News Chen Yang

Shipping is moving to the centre of global commodity trading.

At a time when energy flows, geopolitics, vessel ownership, marine fuels and decarbonisation are all changing at the same time, control over shipping capacity is becoming more important than ever.

Recently, Xinde Marine News Editor-in-Chief Chen Yang spoke with Andrea Olivi, Global Head of Shipping at Trafigura, one of the world’s leading commodity trading companies.

For many years, commodity traders largely relied on the charter market to organise shipping capacity. Cargill is a typical example of this model. It has built one of the world’s leading ocean transportation platforms through chartered tonnage, freight trading and logistics capability, while not owning or crewing the vessels it uses.

But the market environment is changing.

From this interview with Olivi, one message is clear: companies such as Trafigura are reassessing the strategic value of vessel control, bunker supply and shipping resilience. In a more fragmented and uncertain world, the ability to control ships, secure fuel, and keep cargo moving during a crisis is becoming a source of supply chain resilience, customer service capability and market influence.

Olivi joined Trafigura in September 2015. He served as Global Head of Wet Freight from July 2020 to September 2024, and became Global Head of Shipping in October 2024. Before joining Trafigura, he worked at SOCAR Trading and Teekay, with deep experience in tanker chartering, freight trading and shipping asset-related business.

Founded in 1993, Trafigura is one of the world’s major commodity trading houses. Its business covers energy, metals, minerals, bulk commodities and related logistics infrastructure. The company describes itself as a global supply chain platform connecting producers and consumers of critical raw materials and natural resources.

In this interview, Olivi discussed the growth of Trafigura’s shipping business, Chinese shipyards, VLCC newbuildings, the Strait of Hormuz crisis, ships as strategic assets, commodity traders’ control of tonnage, container logistics, bunkering, alternative fuels and global shipping regulation.

A Fleet of around 500 vessels

Olivi recalled that he joined Trafigura around 11 years ago, directly into the shipping department. At the time, he was based in Geneva and worked on chartering, mainly focusing on Aframax and Suezmax vessels in the Mediterranean and Atlantic markets.

When he joined, Trafigura’s shipping book was at an important turning point.

Shipping had historically been seen as more of a cost centre, supporting Trafigura’s internal cargo flows. It then started to evolve into a profit centre. The shipping department expanded its activities through time charters, FFA paper and sale-and-purchase opportunities, while also serving third-party clients outside Trafigura’s own cargo book.

At that time, Trafigura controlled fewer than 100 vessels.

Today, the company controls around 500 vessels across wet and dry shipping.

The shipping team has also expanded significantly. Including front office, middle office and back office functions, Trafigura’s shipping team now has more than 100 people. Its shipping presence spans multiple offices, including Athens, Mumbai, Shanghai, Singapore, Montevideo, Houston, London and Geneva.

Behind this expansion is the rising importance of shipping in global trade.

Olivi said Trafigura’s shipping business used to focus mainly on moving the group’s internal oil, metals and bulk cargoes. Today, more than 60% of its shipping business is with third-party clients. These include Asian refineries, other trading houses, and national oil companies in the Middle East and North Africa.

This means Trafigura’s shipping department has grown from an internal support function into a global shipping operating platform. It serves Trafigura’s own trading system, but is also increasingly serving the wider market.

Why Trafigura ordered VLCCs in China?

Trafigura’s recent moves in the VLCC market have attracted wide attention.

Olivi said Trafigura has ordered more than 10 VLCCs at Chinese shipyards. The recent delivery of its first VLCC from Hantong was an important milestone for the company.

Speaking about Chinese shipyards, Olivi was clear in his assessment.

He said Trafigura had visited the relevant Chinese yards several times and was very pleased with their work. In his view, the growth of China’s shipbuilding industry over the past years has been an “incredible success story”. Leading Chinese yards have reached a very high level of quality, and yards such as Hantong have demonstrated strong building capability.

This also explains why more international shipowners, commodity traders and financial institutions are willing to place large vessel orders in China.

At the same time, Olivi stressed that Trafigura does not see itself as a traditional shipowner.

He said Trafigura has always said it does not want to become a shipowner. But when the right opportunity appears, the company is not afraid to move into asset ownership.

When a company already controls 450 to 500 vessels, owning a small percentage of that fleet can provide significant flexibility. The purpose is not to transform Trafigura into a traditional shipowner, but to optimise its overall freight portfolio and reduce exposure to volatility in the external charter market.

Why VLCCs?

Trafigura’s decision to build VLCCs in China and expand its VLCC exposure through newbuildings and resale opportunities is not accidental.

Olivi believes the VLCC segment has strong future prospects.

The sources of new crude oil growth are changing. More growth is coming from places such as Guyana, Venezuela, Argentina and West Africa. These regions are farther away from Asian consumption markets. As a result, average crude oil sailing distances are increasing.

That means tonne-mile demand is growing. Even if absolute crude consumption changes only gradually, longer trade routes still create additional vessel demand.

In addition, the global VLCC fleet is ageing. Some older vessels have been involved in sanctioned trades or the so-called shadow fleet. As compliance pressure increases, these vessels will eventually need to leave the mainstream market.

These factors, Olivi said, support Trafigura’s interest in VLCCs.

He also noted that refineries and terminals around the world are improving their ability to handle larger ships. More terminals are being dredged or upgraded to accommodate bigger vessels. US exporters are also increasingly willing to use one VLCC instead of several Aframaxes to move the same volume. In general terms, one VLCC can carry roughly the equivalent of three Aframax cargoes.

In a world that continues to pursue efficiency and scale, the economies of scale offered by VLCCs remain highly attractive.

Ships and ports are becoming strategic assets

During Singapore Maritime Week this year, BW Group Chairman Andreas Sohmen-Pao made a striking comment: “Ships are the new chips.”

During the interview, Chen Yang asked Olivi whether he agreed that ships are increasingly being treated as strategic assets in a more fragmented geopolitical environment.

Olivi’s answer was direct.

He agreed — and added ports to the equation. Ships and ports are both becoming increasingly strategic.

In his view, this trend will continue. More countries want to control strategic fleets. The United States has discussed increasing the number of US-flagged vessels it controls. Around the world, more countries and companies are seeking to buy, lease or otherwise control vessels to improve their logistics security.

The Middle East is a particularly clear example. The Strait of Hormuz crisis has reminded national oil companies and energy exporters that without controlled tonnage, it is difficult to provide reliable logistics during a crisis.

This is an important reason why vessel assets are being revalued.

In the earlier phase of globalisation, the market often assumed that ships would always be available on the open charter market. Today, geopolitics, sanctions, war risks, port restrictions and insurance conditions can all affect vessel availability. For energy companies, commodity traders and state-backed platforms, “can I get the ship?” is becoming as important as “what is the freight rate?”

Greater control of shipping capacity

For decades, many cargo owners and commodity traders preferred to control transportation through time charters, voyage charters and freight trading, rather than owning and operating large fleets.

In the past, controlling cargo and chartering capacity was often enough. Today, with geopolitics, route security, fleet ageing and compliance pressure all increasing, some traders are reassessing the strategic value of owning at least part of the asset base.

Chen Yang noted during the interview that Trafigura, Mercuria and other commodity trading houses have recently been ordering, buying or controlling more vessels.

Olivi said this is indeed a trend. However, he also stressed that future control of ships will not always come through equity ownership. Control can come through owned vessels, long-term time charters, leasing structures or other arrangements.

The real question is whether a company can control available tonnage when it matters most.

Olivi also highlighted the role of Chinese leasing companies. He described Chinese leasing as a huge success story. Many of Trafigura’s shipping asset transactions have involved Chinese leasing, and he believes the sector still has significant room to grow.

This point is highly relevant for China’s shipping finance market.

As the strategic value of vessel assets rises, Chinese leasing companies are not only providing financing. They are also participating in the restructuring of global tonnage control. For Chinese shipping finance institutions, future value will come not only from funding cost and transaction structure, but also from their ability to embed themselves in energy trade, logistics security and fleet renewal systems.

The Strait of Hormuz crisis: Seafarer safety comes first

When discussing the Strait of Hormuz crisis, Olivi did not begin with freight rates. He began with seafarer safety.

He told Xinde Marine News that the risk of transiting the Strait of Hormuz should not be viewed only through a financial lens. The industry must also recognise the real risks being carried by seafarers on board. Behind every vessel, every cargo and every commercial transaction are individuals making personal sacrifices to keep global trade moving.

This message was also reflected in a recent public social media post by Olivi.

During Posidonia, Trafigura and TFG Marine hosted a reception in Athens for more than 1,000 guests from across the global maritime community. In that post, Olivi wrote that there was no more fitting place than Athens to reflect on the enduring importance of shipping. Greece has been at the heart of global maritime trade for centuries, and shipping remains one of the essential foundations of the world economy.

Yet amid the industry gathering, he specifically referred to seafarers still stranded in the Arabian Gulf. This, he said, was a powerful reminder that shipping is not only about vessels, cargoes and contracts. The global system is kept running by individual seafarers working under difficult conditions.

Olivi emphasised that the resilience, professionalism and dedication of seafarers are fundamental to the industry. He also called on the industry to support affected crews and help secure their safe passage.

In the interview, he continued this theme.

He said seafarers have paid the price in multiple crises over recent years. The crew change crisis during Covid-19 was one example. Now, in high-risk areas such as the Strait of Hormuz, seafarers are again the people most directly exposed to danger.

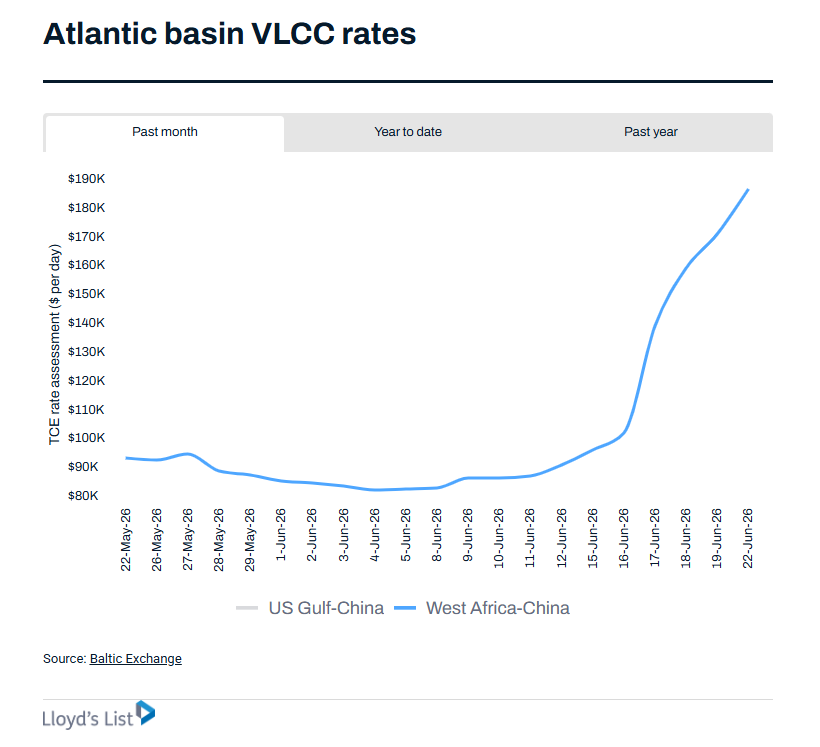

Olivi said that if the Strait of Hormuz can reopen in a safe, organic and orderly way, it would indeed create opportunities for shipping. This would be particularly important for VLCCs and Suezmaxes. If Iranian volumes became available to the international market and could move on international shipping, it would be a major boost to tonne-mile sentiment and freight rates.

But safety comes first.

He said that although transits had recovered somewhat, they were still far below pre-crisis levels. The industry needs to see a stable period with no attacks, no disturbances and no conflicting headlines before it can return to normal.

At the time of the interview, Olivi said Trafigura had multiple vessels affected by the Hormuz situation. At one stage, as many as nine vessels were stuck

This detail shows that even large global trading houses cannot stand outside geopolitical risk. The more global the trading platform, the more it needs strong fleet control, risk management and investment in seafarer safety.

For the shipping market, the reopening of the Strait of Hormuz may represent opportunity. For seafarers, safe passage is the starting point for any recovery.

How long can the VLCC market stay strong?

On the outlook for VLCCs, Olivi said he remains broadly positive for the next two years.

Trafigura has built a VLCC position it is comfortable with. That position can serve Trafigura’s growing internal cargo volumes, while also supporting third-party business.

Olivi believes the VLCC story will remain strong over the next two years. Beyond 2030 and 2031, the answer will depend on how the orderbook develops.

On one side, the global VLCC fleet is old. Some vessels involved in sanctions-related trades or facing compliance issues will need to exit. This creates room for new tonnage.

On the other side, Chinese shipyard margins are strong and capacity is expanding. Some Korean yards are also increasing capacity outside Korea, including in Vietnam and the Philippines. Not all of this capacity will be used for VLCCs, but global shipbuilding capacity is increasing.

Olivi therefore warned that the industry needs to be careful not to overbuild by 2030 or 2031.

When Chen Yang asked whether Trafigura still had interest in buying secondhand VLCCs, Olivi made clear that the company is comfortable with its current position.

This suggests that Trafigura’s VLCC strategy is not an unlimited expansion. It is more about building a controlled, efficient and future-facing tonnage position during a specific market window.

It also reflects an important feature of asset strategy among leading traders. They value assets, but they do not simply chase fleet size. They value control, but they also manage asset exposure. For Trafigura, VLCCs are part of a broader shipping portfolio, not a single bet on one vessel cycle.

Olivi sees another opportunity from China

China’s electric vehicle industry is growing rapidly. Europe and other markets are importing more Chinese electric vehicles. Chen Yang therefore asked whether electrification in the automotive sector could affect oil demand, tanker markets and the VLCC outlook.

Olivi believes global oil demand will continue to grow. Countries such as India will continue to increase oil consumption. Based on studies by organisations such as the IEA, oil demand growth is expected to continue for many years.

At the same time, he said the energy transition will create new shipping opportunities.

In his view, China is positioning itself as an important “electro state”.

He also noted that, when it comes to sourcing green ammonia, China currently offers very competitive prices.

Over the next 20 to 30 years, the pace of oil demand growth may slow. But exports of green ammonia and green methanol from China could create new cargo flows and new vessel demand. Ammonia carriers, for example, may benefit from this transition.

This shows the complex impact of the energy transition on shipping.

It may reduce part of traditional oil shipping demand, but it will also create new energy transportation demand. The industry should not only focus on the decline of one fuel. It also needs to track the emergence of new fuels, new cargoes and new trade flows.

For China, this point is particularly important. Electric vehicles, green power, green methanol, green ammonia and new energy equipment exports may together reshape future seaborne demand. The shipping industry needs to move beyond the narrow question of whether crude oil demand will fall, and look at the broader restructuring of global energy trade.

Is Trafigura entering container shipping?

Some recent reports suggested that Trafigura wants to grow in the container space.

During the interview, Xinde Marine News asked whether this meant Trafigura would time charter container ships, or even order new containerships.

Olivi said the company has no current plans to do so.

He said the growth in Trafigura’s container business mainly reflects the increasing number of containers the company moves around the world through freight forwarding. For example, as Trafigura trades and moves more concentrates and other cargoes, its container logistics needs naturally increase.

As a result, Trafigura has taken a container business that was previously handled in a more decentralised way by operations, and created a centralised container chartering unit. The logic is similar to how the company manages oil and dry bulk freight.

But Olivi made clear that he does not expect Trafigura to time charter container ships in the near future, nor order any containerships.

This means Trafigura’s container focus is on freight organisation and logistics management, not entering the liner shipping or containership ownership market.

This also helps define the boundaries of Trafigura’s shipping strategy. The company will strengthen logistics organisation around its own trade flows and customer needs. But its approach to asset control differs across vessel types and business segments. Tankers and dry bulk carriers are closely linked to core commodity flows. Container business, for now, is more about logistics management and internal efficiency.

Bunkering is also becoming a strategic capability

When discussing TFG Marine, Olivi said bunkering is becoming increasingly strategic.

TFG Marine is an important bunkering platform founded by Trafigura. Public information shows that in May 2026, CMB.TECH increased its stake in TFG Marine from 10% to 15%. After the adjustment, TFG Marine’s shareholding structure became Trafigura 70%, Frontline Management AS 15% and CMB.TECH 15%. Trafigura’s announcement also quoted Olivi as saying that TFG Marine has become one of the world’s leading marine fuel supply platforms, built on operational capability, digitalisation, modernisation and transparency.

In the interview, Olivi explained the value of bunkering in simple terms.

If a vessel cannot be bunkered, it cannot sail. Therefore, bunkering itself is part of shipping security.

The Strait of Hormuz crisis also showed that without the right bunkering setup and supply chain, a crisis can lead to fuel shortages and sharply higher bunker premiums at certain locations.

For shipowners, bunker risk is not only a price risk. It is also a quality and operational risk.

Olivi gave an example. If an eco Capesize is earning around $60,000 to $65,000 per day, the last thing a shipowner wants is for off-specification fuel to be put on board, forcing the ship to stop for five days to de-bunker.

This is one reason why more shipowners are willing to participate in, or align with, high-quality bunkering platforms.

Fuel supply is no longer just a procurement cost issue. It affects vessel availability, compliance, earnings and risk management. For large traders and shipowners, the stability of the bunker supply chain is becoming part of shipping capability.

In the past, the market focused mainly on who controls the ship. Today, it also needs to ask: who can provide reliable fuel at key ports? Who can guarantee fuel quality? Who can maintain supply continuity during a crisis? These questions are raising the strategic value of bunkering platforms.

A multi-fuel future: bunker platforms must become supermarkets

On future marine fuels, Olivi believes the industry will move into a multi-fuel environment.

Speaking from the perspective of TFG Marine, he used a simple analogy: a bunker platform must be like a supermarket. If a customer wants LNG, the platform needs to supply LNG. If a customer wants methanol or ammonia, the platform needs to be able to supply those fuels as well.

But different fuels will scale at different speeds.

Olivi believes hydrogen-based fuels such as green ammonia and green methanol will take more time. They remain expensive. Without the right regulatory framework and fee-based systems, these fuels will find it difficult to gain large-scale market share quickly.

Biofuels may be easier to scale in the near term.

He also pointed to ethanol as an interesting emerging fuel. Some methanol engines are already testing ethanol blends. The next few years will be important in determining whether ethanol can also scale.

This view is consistent with what the shipping industry is experiencing. Shipowners can no longer easily bet on a single fuel pathway. LNG, methanol, ammonia, biofuels and ethanol are all trying to find commercial space.

For bunker suppliers, this means future capability cannot be built around only one fuel. Competition will increasingly depend on who can offer a multi-fuel portfolio, who can build compliant, reliable and traceable fuel supply chains across regions, and who can help owners and charterers balance cost, compliance and availability.

FuelEU Maritime is more effective than EU ETS — but global rules matter more

On regulation, Olivi made a distinction between EU ETS and FuelEU Maritime.

He said that, based on conversations with shipowners, FuelEU Maritime does more to drive investment in green technology than EU ETS. EU ETS is more like an additional tax on fossil fuel consumption. FuelEU Maritime has a more direct influence on fuel choice and long-term investment decisions by owners and charterers.

The problem is that FuelEU Maritime remains a regional measure.

Olivi believes meaningful change in shipping requires a global framework. The continued layering of regional measures makes compliance increasingly complex for shipowners and market participants.

He also noted that there had been discussions in the market about whether China might one day consider a similar mechanism to FuelEU Maritime. But he remains sceptical about the growing number of regional measures around the world.

In his view, a global framework would be preferred and would better support long-term investment decisions.

This is one of the central challenges facing green shipping. Shipowners, traders, charterers and fuel suppliers all need to make long-term investments, but the regulatory path is still evolving. Regional rules can help push the market forward, but without global alignment, companies must constantly balance different rules, regions and fuel standards.

For a global company such as Trafigura, a unified, clear and predictable regulatory framework is more useful for long-term investment than an expanding patchwork of regional requirements.

The next five years of Trafigura

Looking ahead to the next five years, Olivi said Trafigura’s first priority is to consolidate its existing fleet.

Managing around 500 vessels is already a highly complex task. Trafigura needs to keep strengthening its organisation, risk management and operational efficiency.

At the same time, Trafigura wants to continue growing its shipping business. This includes serving the group’s expanding internal oil, metals and bulk commodity flows, while also developing more third-party business.

Olivi specifically mentioned Asian customers and Chinese refineries as areas where Trafigura wants to grow.

This shows that Trafigura’s shipping business will continue to serve its own trading system, while also playing a more independent role in the global shipping market.

This follows the evolution of Trafigura’s shipping business over the past decade: from internal cost centre, to profit centre, to global shipping operator serving external customers. As third-party business increases, Trafigura’s shipping capability is no longer only an internal support function. It has become part of the company’s external service capability and market influence.

China’s opportunity: shipyards, leasing, green fuels and customers

China appeared repeatedly in this interview.

Chinese shipyards have become important partners in Trafigura’s large-vessel strategy. Chinese leasing has participated in some of Trafigura’s shipping asset transactions. Chinese refineries are important customers that Trafigura wants to further develop. China’s potential supply of green ammonia and green methanol is also viewed by Olivi as an opportunity.

Taken together, China plays more than one role in Trafigura’s shipping map.

The value of vessel assets is being repriced

This interview sends a clear signal: vessel assets are being repriced within the global trade system.

In the past, ships were often viewed mainly as cyclical assets. Today, they are also supply chain security assets, energy security assets, financial assets and compliance assets.

For a global commodity trader such as Trafigura, controlling ships is not only about earning from freight volatility. It is about cargo flows, customer service, risk management, bunker supply, compliance capability and crisis response.

Olivi’s comments also help explain a wider industry phenomenon: why global newbuilding orders and secondhand vessel transactions remain active even when newbuilding prices are high, yard slots are tight and alternative fuel pathways remain uncertain.

For leading traders, energy companies, state-backed platforms, financial capital and major shipowners, future ships can no longer be viewed only through the old lens of freight cycles.

Ships are moving from efficiency tools to security tools.

This is why the phrase “ships are the new chips” has resonated across the shipping industry. Ports, fleets, bunkering, leasing and green fuel supply chains are together becoming part of the new infrastructure of global trade.

Trafigura’s roughly 500-vessel fleet, VLCC newbuildings, cooperation with Chinese shipyards, TFG Marine bunkering platform and multi-fuel strategy are all examples of this trend.

In a more uncertain world, shipping capability is no longer simply the ability to move cargo from point A to point B. It is becoming a core capability for commodity traders, energy companies and national industrial systems to protect supply chains, manage risk and serve customers.

That is the real change behind Trafigura’s growth from fewer than 100 controlled vessels to around 500. Vessel assets, port access, fuel supply, leasing structures and green fuels will together shape the next stage of global shipping competition.

READ MORE

Tankers

Tankers

20-Year-Old VLCC Fetches $50M – Market Logic Turned Upside Down

Tankers

Tankers

First Ammonia-Fuelled Ship Loads Green Ammonia in China

Tankers

Tankers

WS 897! A Single VLCC Voyage Could Earn $30 Million: How Sinokor Capitalized on Persian Gulf Risks for an Astronomical Premium

Tankers

Tankers

Fratelli Cosulich Takes Delivery of Second Methanol-Ready Bunker Tanker

Tankers

Tankers

The Second Surge: How Geopolitics and the Strait of Hormuz are Rewriting VLCC Freight Rates

Tankers

Tankers