Shipbuilding Orders Surge: Is 2026 Becoming Another 2008?

Contracting volumes in the current six-year cycle are set to exceed those recorded before the 2008 crash, but the size of the fleet, the age profile of existing vessels and the structure of shipyard capacity point to a very different market

A familiar question is returning to the centre of the global shipping debate: is 2026 becoming another 2008?

Newbuilding prices remain elevated. Delivery slots at leading yards extend into 2029 and 2030. Orders continue to flow across containerships, tankers, gas carriers and large bulkers. At the same time, Chinese shipyards are expanding capacity, while several previously inactive or restructured facilities are re-entering the market.

For shipping executives who experienced the last super-cycle, the parallels are difficult to ignore.

A new analysis from Maritime Strategies International suggests that the similarities are real. Yet the underlying market structure is very different from the one that preceded the 2008 crash.

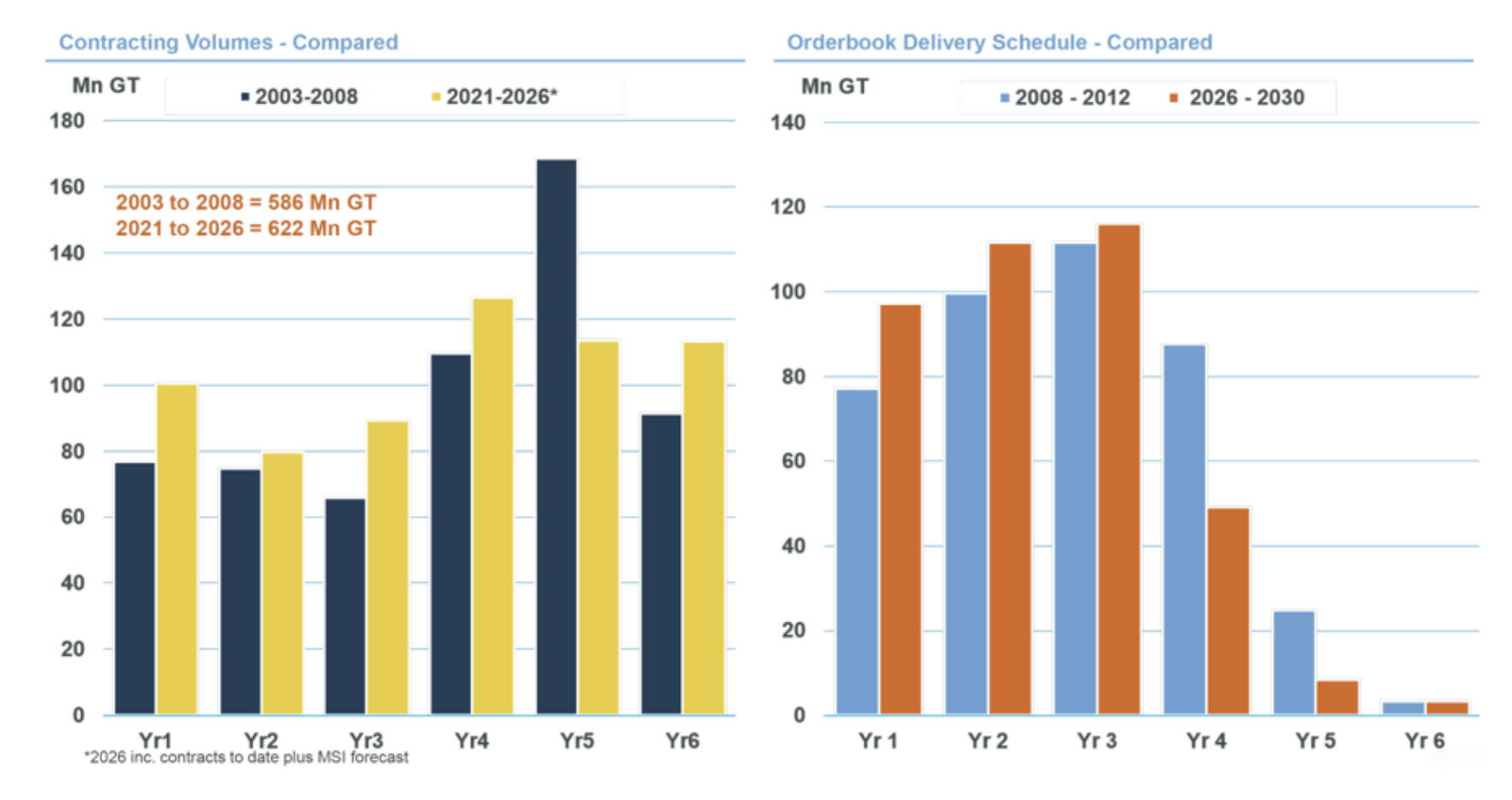

Contracting volumes are remarkably similar

MSI managing director Adam Kent recently compared global shipyard contracting between 2003–2008 and 2021–2026 during a presentation at Marine Money Week in New York.

MSI estimates that shipyards secured about 586 million gross tonnes of orders between 2003 and 2008. For the 2021–2026 period, including MSI’s forecast for the remainder of this year, total contracting is expected to reach approximately 622 million gross tonnes.

On that basis, the current six-year ordering cycle will exceed the total contracted tonnage recorded during the run-up to the global financial crisis.

The annual contracting profiles also look strikingly similar. Both cycles moved through an initial expansion phase, accelerated in the middle years and then remained at historically high levels.

The delivery schedules add another reason for caution. MSI’s comparison suggests that today’s orderbook is slightly more front-loaded than the one in place in 2008. A greater proportion of the current backlog is scheduled for delivery during the first three years.

That means the market may feel the impact of rising fleet supply sooner than some owners expect.

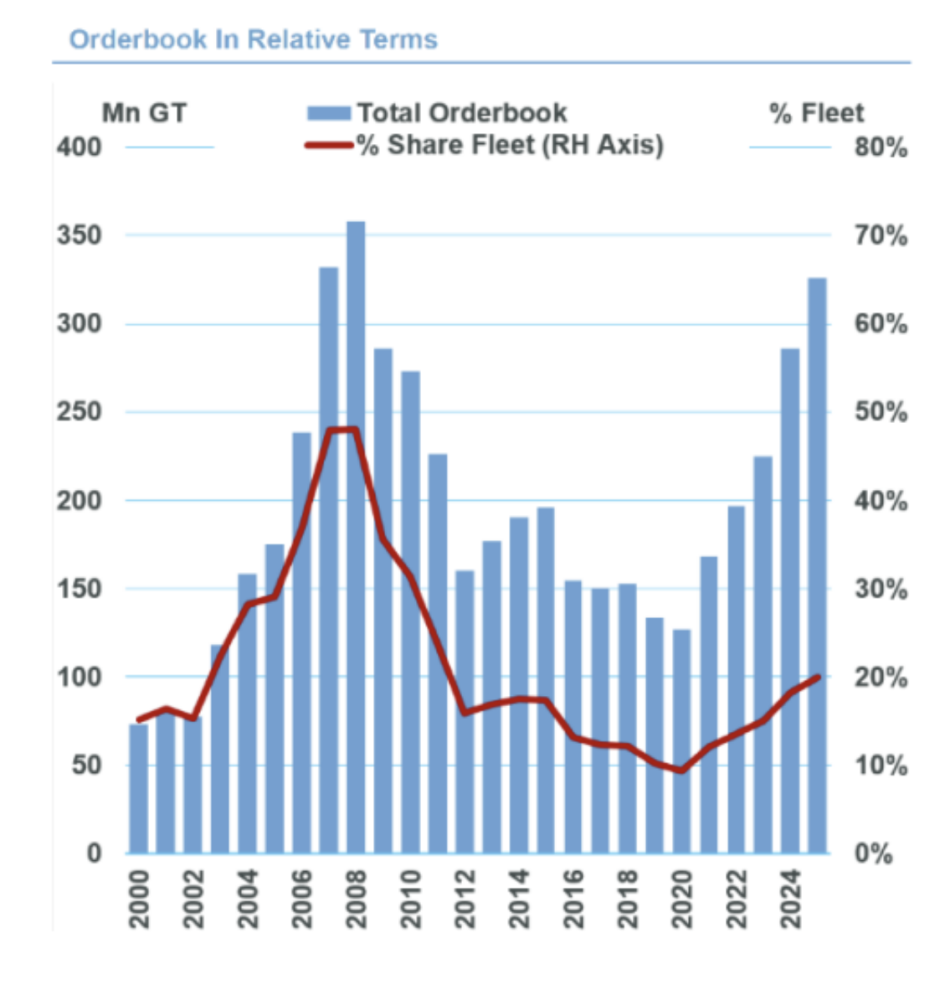

The biggest difference is the denominator

Absolute contracting volumes tell only part of the story.

The global merchant fleet is now much larger than it was in 2008. According to MSI, today’s orderbook is equivalent to around 20% of the fleet already on the water. In 2008, the corresponding figure was approximately 50%.

In practical terms, the 2008 market had roughly one vessel on order for every two vessels in service. That level of supply growth left the industry extremely exposed when trade and financing conditions deteriorated.

Today’s orderbook is large, but its relative impact on the existing fleet is far smaller.

Xinde Marine News reached a similar conclusion in a 2026 analysis of newbuilding prices and the current shipbuilding cycle. Based on the methodology used in that report, the global orderbook represented around 15% of the fleet, compared with about 50% in 2008.

The difference between 15% and 20% reflects variations in vessel coverage, measurement periods and tonnage definitions. The broader conclusion is unchanged: the current orderbook is substantial, but it has not reached the extreme relative scale seen before the 2008 downturn.

Shipyard capacity also looks different.

Xinde Marine News previously reported that current global shipbuilding capacity is equivalent to roughly 5% of the fleet, compared with about 14% in 2008.

During the previous super-cycle, new yards entered the market rapidly and capacity expanded alongside ordering. Today, effective capacity is still constrained by dock availability, skilled labour, engineering resources, equipment supply, project management and the ability to build increasingly complex vessels.

The scarce resource is no longer simply physical yard space. It is the ability to deliver high-specification, fuel-efficient and alternative-fuel vessels on time.

An older fleet provides a buffer

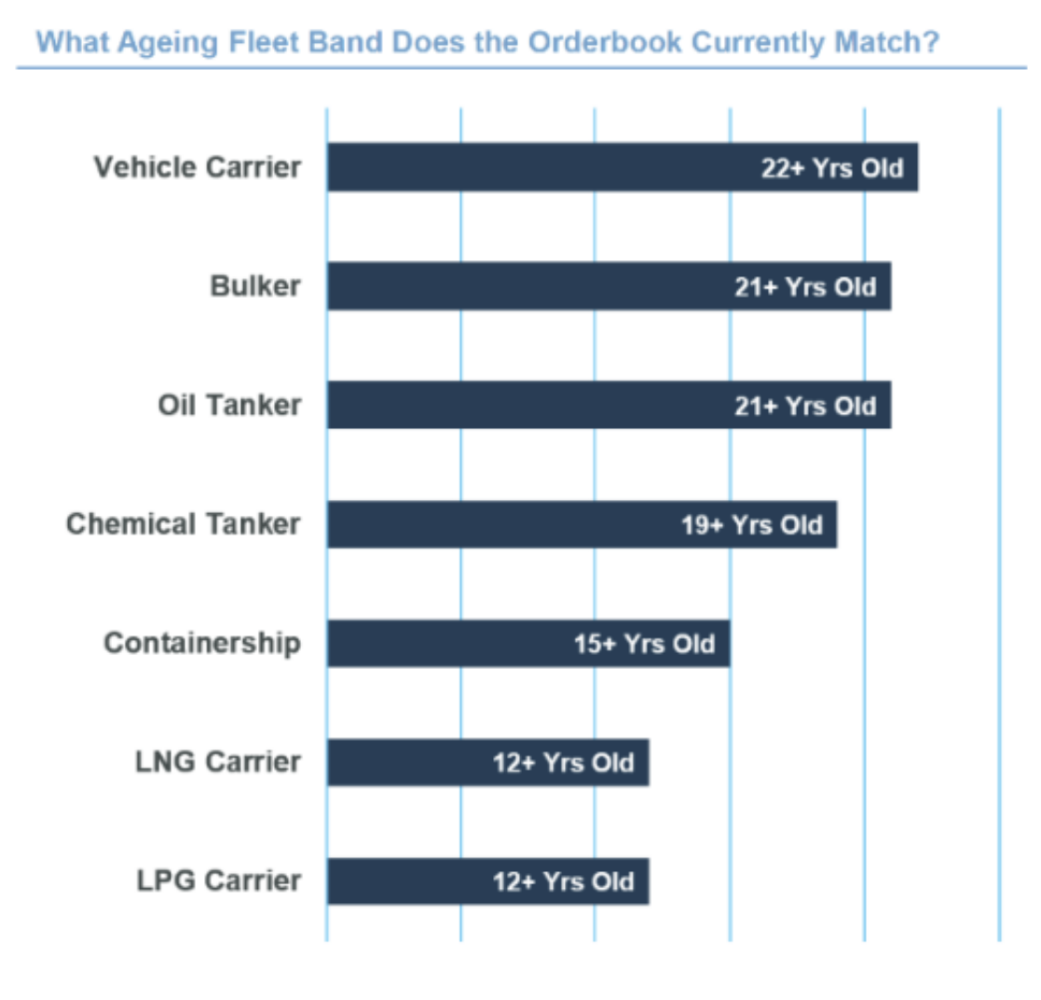

MSI’s latest analysis also compares the orderbook in each major shipping sector with the volume of ageing tonnage already in service.

The results show that the current vehicle carrier orderbook is broadly equivalent to the entire fleet aged 22 years and above.

For bulk carriers and oil tankers, the orderbook is equivalent to vessels aged 21 years and above. For chemical tankers, the comparable age threshold is 19 years. For containerships, it is 15 years.

LNG carriers and LPG carriers present a different picture. In both sectors, the orderbook is broadly equivalent to all vessels aged 12 years and above.

This age comparison is important because the global fleet entering the current cycle is older than the fleet that entered the 2008 downturn.

Before 2008, a large share of ordering was driven by pure fleet expansion. Today, a meaningful proportion of newbuilding investment is linked to replacement.

Many vessels delivered during the 2008–2012 construction wave are now moving into the 15-year-plus age bracket. Owners must assess rising maintenance costs, fuel efficiency, carbon exposure, financing terms, charterer requirements and residual values.

Xinde Marine News reported earlier this year that Arrow Shipbroking Group expects the global market to require around 46,000 new vessels over the next 15 years. Fleet ageing is one of the main reasons behind that forecast.

For some sectors, this replacement requirement could absorb a significant share of the current orderbook.

MSI argues that vehicle carriers, for example, have enough ageing tonnage to reduce future oversupply through scrapping if market conditions weaken sharply.

The position is less comfortable for LPG carriers. MSI remains positive on LPG trade growth, which supports the large orderbook. If demand underperforms, however, the relatively young fleet and heavy delivery schedule could become a more serious concern.

Scrapping capacity does not guarantee scrapping

An ageing fleet creates room for supply adjustment, but it does not ensure that old vessels will leave the market.

Strong freight rates, Red Sea diversions, sanctions trading, longer energy routes and regional conflicts have extended the commercial lives of many older ships.

As long as an ageing vessel continues to generate attractive cash flow, owners have little incentive to recycle it.

Xinde Marine News previously estimated that global recycling activity remained at only around 5 million to 6 million compensated gross tonnes per year between 2023 and 2025. That is a modest figure relative to the size of the world fleet.

Low recycling volumes have not removed replacement demand. They have postponed vessel exits.

MSI’s suggestion that some sectors could “scrap their way out” of an oversupply problem should therefore be understood as available adjustment capacity rather than a guaranteed market outcome.

Actual recycling decisions will depend on freight earnings, scrap prices, environmental regulations, financing conditions, insurance requirements and charterers’ age restrictions.

If geopolitical disruption continues to absorb capacity, older vessels may remain in service. The market could then face rising newbuilding deliveries without a corresponding increase in demolition.

That combination would create pressure even in sectors with a large pool of ageing ships.

Today’s orders serve a broader strategic purpose

The investment rationale behind the current ordering cycle is also more complex than it was before 2008.

The previous boom was driven primarily by strong freight markets, rapid trade growth, easy financing and expectations of further asset appreciation.

Those factors still matter, but owners today are also investing to improve energy efficiency and prepare for tighter environmental regulation.

The EU Emissions Trading System, FuelEU Maritime and future global greenhouse gas rules are widening the operating-cost gap between modern and inefficient vessels.

Cargo owners are also placing greater value on access to reliable transport capacity. Governments increasingly view shipping as part of national energy, trade and supply-chain security. Large shipping groups are using newbuildings to secure future capacity, fuel optionality and operational flexibility.

During Singapore Maritime Week 2026, Xinde Marine News examined this shift through the idea that “ships are the new chips”.

Under this framework, vessels, ports, seafarers, bunkering systems and transport corridors are becoming strategic assets. Their value increasingly reflects resilience, compliance and deployability, as well as freight earnings.

This helps explain why some newbuilding projects can proceed even when their economics appear less compelling against current charter rates.

A vessel supported by long-term cargo, efficient propulsion, strong financing and strategic employment may still justify investment at a high purchase price.

The risk is building beyond 2028

None of these structural differences eliminates the danger of oversupply.

The current delivery schedule is heavily weighted towards the next several years. New Chinese capacity is also moving closer to commercial production. Reopened yards are winning contracts, while established shipbuilding groups continue to invest in docks, production lines and supporting infrastructure.

Previous analysis cited by Xinde Marine News indicated that global shipbuilding capacity could rise from around 30 million CGT in 2020 to approximately 67 million CGT by 2028, with much of the increase concentrated in China.

This expansion should gradually ease the shortage of berths. It could also place pressure on newbuilding prices and shipyard margins.

The larger risk would emerge if several developments occur at the same time.

New ordering could remain high. Additional yard capacity could enter production as planned. Recycling could stay weak. Meanwhile, Red Sea diversions, sanctions-related inefficiencies and other geopolitical disruptions could begin to unwind.

Under that scenario, effective fleet supply would increase rapidly.

The exposure will vary by sector.

Vehicle carriers have a relatively large pool of ageing tonnage that could be removed. Bulk carriers and tankers also retain some replacement capacity.

Large containerships, LNG carriers and LPG carriers are more dependent on future trade growth, project start-ups and network changes to absorb their orderbooks.

The industry therefore faces a fragmented outlook rather than a single global supply cycle.

2026 is not yet 2008

The current market shares several visible characteristics with the years preceding the 2008 crash.

Contracting is historically high. Newbuilding prices remain elevated. Delivery schedules are becoming concentrated. Shipyard capacity is expanding, and confidence among owners remains strong.

The underlying structure, however, is different.

The orderbook is much smaller relative to the fleet. Effective yard capacity is lower relative to the fleet. Existing vessels are older. Environmental regulation is creating genuine replacement demand. Owners and cargo interests are also attaching greater strategic value to modern tonnage.

For these reasons, 2026 is not a straightforward repeat of 2008.

The present cycle has a stronger replacement foundation and a broader strategic rationale. Those buffers are meaningful, but they are not unlimited.

Over the next two to three years, the direction of the market will depend on the interaction between newbuilding deliveries, shipyard expansion, vessel recycling and the amount of capacity absorbed by geopolitical disruption.

The key indicators are no longer contracting volumes and newbuilding prices alone.

The industry must also watch the orderbook-to-fleet ratio, the actual output of new and reactivated yards, the pace of demolition and the extent to which longer routes and disrupted trade patterns continue to absorb ships.

The 2008 crisis emerged when ordering and shipyard capacity expanded beyond the market’s ability to absorb them.

The industry has not reached that point in 2026. The warning signs, however, are becoming harder to ignore.

READ MORE

Shipbuilding

Shipbuilding

MSC Makes PCTC Newbuilding Debut with 12-Ship China Programme

Shipbuilding

Shipbuilding

ADNOC L&S Returns to Jiangnan with $900m LNG Carrier Order

Shipbuilding

Shipbuilding

The Greek owner has booked three 1,800-teu Bangkokmax vessels at China Merchants’ Qingshan Shipyard

Shipbuilding

Shipbuilding

ADNOC L&S Expands LNG Fleet with $900m Order for Four New Carriers

Shipbuilding

Shipbuilding

Container Shipping’s Supply Paradox: Ships Are Scarce Today, but Nearly 5 Million TEU Could Arrive in 2028

Shipbuilding

Shipbuilding

Liaoning Port Moves to Add Two 5,200-hp Electric Tugs

Shipbuilding

Shipbuilding

SunRui Secures Rotor Sail Systems for Two Vessels, Deliveries to Begin in 2027

Shipbuilding

Shipbuilding

Dajin Heavy Industry Lands New Shipbuilding Orders, Parent Provides Guarantees

Shipbuilding

Shipbuilding

China's Largest Full-Revolving Semi-Submersible Crane Vessel Delivered in Jiangmen

Shipbuilding

Shipbuilding