MSC Makes PCTC Newbuilding Debut with 12-Ship China Programme

The world’s largest container line is extending its maritime asset strategy beyond boxships, with MSC-owned Global Car Carriers assembling a 12-vessel LNG dual-fuel PCTC orderbook at three Chinese shipyards.

Mediterranean Shipping Company has made its clearest move yet into car-carrier newbuildings, with its vehicle-carrier investment platform GCC Global Car Carriers listing 12 large LNG dual-fuel pure car and truck carriers under construction in China.

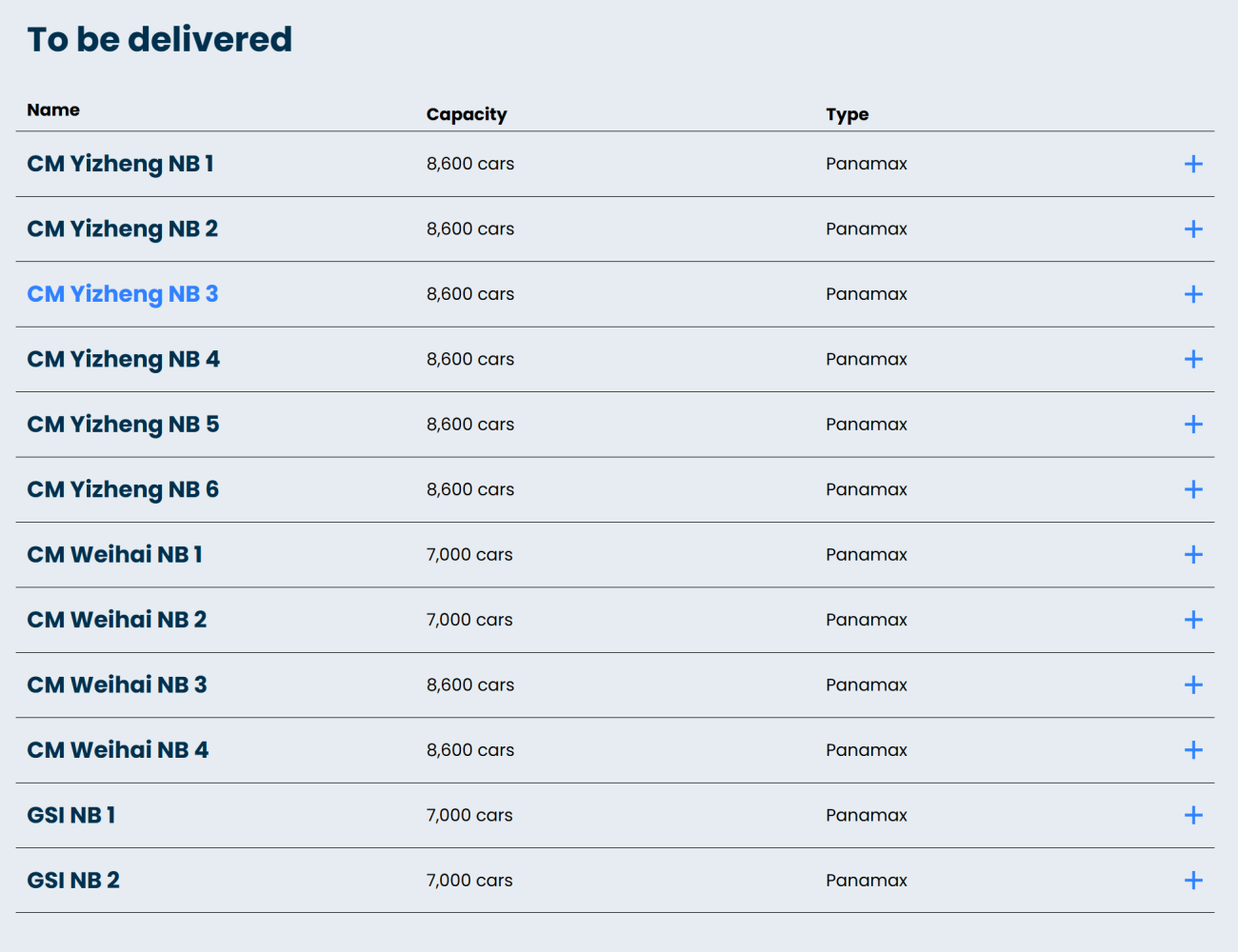

According to GCC’s latest fleet list, the programme comprises eight 8,600-ceu vessels and four 7,000-ceu ships for delivery between 2028 and 2030.

China Merchants’ Yizheng facility will build six of the 8,600-ceu ships. China Merchants Weihai is responsible for two 8,600-ceu vessels and two 7,000-ceu units, while Guangzhou Shipyard International will construct the remaining two 7,000-ceu ships. All 12 are listed as LNG dual-fuel vessels.

The newbuildings will significantly reshape GCC’s fleet. The company currently lists 20 trading vessels and 12 ships to be delivered, taking its combined operating and orderbook fleet to 32 units. Once the programme is completed, Panamax and large PCTCs will represent the majority of its controlled tonnage.

No contract values have been disclosed. A benchmark 7,000-ceu LNG-ready PCTC was still priced at around $90m in late 2025, suggesting that GCC’s larger and more highly specified programme is likely to represent an investment comfortably above $1bn.

The significance of the move extends beyond the number of ships involved. MSC has moved from acquiring an established car-carrier tonnage provider to backing a substantial fleet-renewal and expansion programme, giving the group a long-term position in a specialised shipping segment outside its core container business.

From acquisition to fleet expansion

GCC was formerly known as Gram Car Carriers, an Oslo-listed PCTC owner whose business model centred on owning vessels and chartering them to global and regional car-carrier operators.

MSC entered the sector in 2024 through its wholly owned subsidiary SAS Shipping Agencies Services, offering NOK263.69 per share for Gram Car Carriers. The transaction was completed in July 2024, with MSC’s subsidiary holding approximately 97.81% of the company before proceeding with compulsory acquisition and delisting. At the time, Gram Car Carriers described itself as the world’s third-largest PCTC tonnage provider.

The company was subsequently renamed Global Car Carriers, preserving the GCC initials while giving the business a more international identity under MSC ownership.

GCC is structurally different from operators such as Wallenius Wilhelmsen, Höegh Autoliners, NYK, “K” Line or Grimaldi, which organise liner-style vehicle-shipping networks and provide wider automotive logistics services.

Its principal role remains that of a shipowner and tonnage provider. It owns PCTCs and places them with established operators under charter arrangements, allowing MSC to gain exposure to the car-carrier market without immediately launching a competing global PCTC service under the MSC brand.

That distinction is important. MSC has acquired a specialist asset platform with established commercial relationships, technical knowledge and access to automotive-shipping customers. The 12-vessel orderbook now adds scale, younger tonnage and lower-emission capability to that platform.

PCTC ordering is returning—but on different terms

The GCC programme comes as car-carrier contracting begins to recover after a sharp slowdown in 2025.

PCTC ordering surged between 2021 and 2024 as charter rates rose to exceptional levels, China’s vehicle exports accelerated and operators struggled to find sufficient modern tonnage. The industry responded with one of the largest fleet-renewal cycles in its history.

Ordering then dropped sharply as owners began to focus on the volume of ships already scheduled for delivery. Depending on the database and cut-off date, only around eight or nine new PCTCs were contracted globally in 2025, the lowest annual total since 2020.

Activity has picked up again in 2026. A review by Xinde Marine News of Clarksons data and publicly disclosed projects indicates that approximately 31 car carriers have been ordered so far this year, with Chinese yards securing about 29 of them.

Beyond GCC, recent projects include two 3,000-ceu multifuel battery-hybrid vessels ordered by UECC, four 1,380-ceu LNG dual-fuel ships for “K” Line’s European short-sea network, two additional 7,000-ceu LNG dual-fuel PCTCs for Zodiac Maritime, and further orders linked to Neptune Lines and Sallaum Lines.Detail:https://www.linkedin.com/pulse/over-yet-16-new-pctc-orders-signal-continued-demand-car-yang-chen-%E9%99%88%E6%B4%8B--iwwoc/

The latest cycle is more selective than the broad ordering wave seen earlier in the decade. New contracts are increasingly linked to defined trades, long-term charter requirements, automotive customers or regional logistics networks.

Technical specifications are also becoming more demanding. LNG dual-fuel propulsion, battery-hybrid systems, methanol capability, ammonia-ready notation, shore-power connections, flexible decks and increased High & Heavy capacity are moving from optional features to central elements of new PCTC designs.

GCC’s choice of 7,000-ceu and 8,600-ceu ships points towards deep-sea employment with major global operators rather than niche regional distribution. The programme is designed around scale, fuel flexibility and the ability to carry a broader mix of passenger vehicles, commercial vehicles and heavy rolling cargo.

The supply risk has not disappeared

Renewed contracting should not be confused with the start of another unrestricted ordering boom.

AXSRoRo data reviewed by Xinde Marine News show that global PCTC deliveries rose from just 12 ships in 2023 to 46 in 2024 and a record 75 in 2025. The market received 133 new ships over those three years, adding close to 1m ceu of capacity.

A further 67 vessels are scheduled for delivery in 2026, followed by 50 in 2027 and 26 in 2028.

Scrapping has remained extremely limited. No PCTCs were demolished in 2024, while only a small number left the fleet in 2025. Unless recycling accelerates, new supply will continue to outpace the removal of older ships.

The orderbook is also heavily concentrated in China. Of the 276 PCTCs delivered or scheduled for delivery between 2023 and 2028, AXSRoRo data indicate that 219—almost 80%—are being built at Chinese yards.

The market is therefore entering a period in which fleet quality may become more important than simple access to tonnage.

Older ships with weaker fuel efficiency, limited deck flexibility or poorer emissions performance are likely to face increasing competitive pressure. New vessels tied to long-term cargo, major charterers and lower-emission logistics requirements should be better positioned, even if overall fleet utilisation softens.

China’s automotive and machinery exports remain an important demand driver. Vehicle manufacturers are continuing to expand sales in Europe, Latin America, the Middle East, Southeast Asia and Oceania, while exports of excavators, loaders, cranes, agricultural equipment and commercial vehicles are increasing the role of High & Heavy cargoes in PCTC employment.

However, rising Chinese exports partly reflect a redistribution of global automotive manufacturing and trade rather than equivalent growth in worldwide vehicle consumption. If ship deliveries continue to outpace cargo growth, freight and charter markets will remain exposed to downward pressure.

MSC’s 1,000-ship container platform

GCC’s expansion needs to be viewed in the context of MSC’s much larger maritime asset strategy.

MSC became the first container line to operate 1,000 ships in 2026. Alphaliner placed its operated capacity at approximately 7.32m teu, around 2.67m teu ahead of second-ranked Maersk.

MSC built that position through a combination of secondhand acquisitions, large newbuilding programmes, chartered tonnage and investments in regional operators. Its fleet now spans small feeder vessels, classic Panamax ships, large mainline tonnage and ultra-large containerships.

The scale has allowed MSC to operate independently following the end of the 2M alliance, deploying its own ships across east-west trades, north-south routes, regional services and feeder networks.

The group has also invested extensively beyond ships, including container terminals, rail assets, inland logistics, towage and regional transport businesses. The result is a system in which vessel capacity, port access and inland distribution can support one another.

Once MSC had established the world’s largest and most diversified container fleet, it began applying its capital and asset-management capabilities more visibly to specialist shipping segments.

Moving into VLCCs

The tanker sector has become another part of that expansion.

A Cyprus filing disclosed in March 2026 showed that MSC, through SAS Shipping Agencies Services, planned to acquire a 50% stake in South Korea’s Sinokor. The transaction would give MSC joint control alongside Sinokor’s existing shareholder, Ga-Hyun Chung.

Sinokor has rapidly become a major force in the very large crude carrier market through a series of vessel acquisitions. Its expansion has provided MSC with an entry into crude transportation through an established platform with its own management, market expertise and operating relationships.

Market reports have also linked MSC to a possible eight-vessel VLCC newbuilding programme at Hengli Heavy Industry, although neither MSC nor the shipbuilder has formally confirmed the contracts.

The pattern resembles the GCC transaction. Rather than building a specialist operation from the ground up, MSC is acquiring stakes in or control of established shipping platforms and then using its capital strength to support further fleet expansion.

PCTCs add another layer to the portfolio

The car-carrier strategy is now further advanced at the newbuilding level.

MSC acquired GCC with an existing portfolio of PCTC assets and charter relationships. The 12 ships now listed at Chinese yards will increase the platform to 32 vessels and shift its fleet towards larger, younger and LNG dual-fuel tonnage.

The potential commercial links are substantial.

MSC already serves many of the world’s largest automotive manufacturers through its container, terminal and inland-logistics networks. GCC adds access to specialised roll-on/roll-off assets capable of carrying finished vehicles, commercial units and heavy machinery on deep-sea routes.

Maintaining GCC as a tonnage provider also gives MSC strategic flexibility. The ships can continue to be chartered to established PCTC operators, generating long-term contracted income without requiring MSC to create a new global car-carrier liner network.

At the same time, MSC’s scale can support GCC through ship finance, insurance, technical management, crewing, fuel procurement, digital systems and relationships with automotive customers.

This structure offers exposure to both the operating and asset sides of the automotive supply chain while limiting the immediate commercial risks of entering a specialised liner market directly.

From container carrier to diversified maritime group

Container shipping remains the foundation of MSC’s business. Its 1,000-ship fleet and more than 7.3m teu of capacity provide the network, capital base and customer reach behind the group’s wider strategy.

The move into VLCCs and PCTCs shows that MSC is extending those capabilities into sectors with different cargoes, earnings cycles and customer structures.

Crude tankers provide exposure to global energy flows. Car carriers connect the group to the expanding international trade in vehicles and heavy equipment. Both segments also offer long-lived physical assets that can generate charter income independently of container freight markets.

GCC’s 12-vessel Chinese newbuilding programme is therefore more than a fleet-renewal exercise. It marks MSC’s transition from buying an established PCTC platform to actively shaping its future fleet.

The timing is significant. The car-carrier market faces a heavy delivery schedule and growing concerns about excess capacity, yet MSC is committing to large, modern and lower-emission tonnage.

That suggests a strategy focused less on short-term charter-market momentum and more on long-term access to automotive cargo, high-quality marine assets and integrated logistics capability.

For Chinese shipbuilders, the programme reinforces their position at the centre of the global PCTC market. For MSC, it adds another specialist fleet to a maritime portfolio that is becoming far broader than container shipping alone.

READ MORE

Shipbuilding

Shipbuilding

The Greek owner has booked three 1,800-teu Bangkokmax vessels at China Merchants’ Qingshan Shipyard

Shipbuilding

Shipbuilding

Container Shipping’s Supply Paradox: Ships Are Scarce Today, but Nearly 5 Million TEU Could Arrive in 2028

Shipbuilding

Shipbuilding

Liaoning Port Moves to Add Two 5,200-hp Electric Tugs

Shipbuilding

Shipbuilding

ADNOC L&S Returns to Jiangnan with $900m LNG Carrier Order

Shipbuilding

Shipbuilding

SunRui Secures Rotor Sail Systems for Two Vessels, Deliveries to Begin in 2027

Shipbuilding

Shipbuilding

Dajin Heavy Industry Lands New Shipbuilding Orders, Parent Provides Guarantees

Shipbuilding

Shipbuilding

China's Largest Full-Revolving Semi-Submersible Crane Vessel Delivered in Jiangmen

Shipbuilding

Shipbuilding

Hengli ’s First-Half Profit Surge as Newbuilding Orders Reach 207 Vessels

Shipbuilding

Shipbuilding

CATL’s Electric Ship Arm Takes Stake in Jiangsu Kaiyang Shipbuilding

Shipbuilding

Shipbuilding