Methanol Orders Stall as LNG’s Transition Window Looks Set to Run Longer

Clarksons data shows 173 LNG-capable vessels ordered in the first half of 2026, while methanol contracting slowed to just four ships

Halfway through 2026, the shipping industry’s fuel transition is showing a much clearer divide.

New orders for methanol-fuelled vessels, one of the most closely watched segments of the alternative-fuel market in recent years, have almost ground to a halt. Ammonia and hydrogen remain confined to a small number of early projects. LNG, meanwhile, continues to dominate alternative-fuel newbuilding activity, particularly in the containership and car carrier sectors.

The shift reflects a broader reassessment of technology risk, fuel availability and lifecycle economics. With the global regulatory framework still unsettled, owners are placing greater value on fuels that are commercially available, supported by existing infrastructure and capable of evolving as emissions requirements tighten.

Andrea Lazzaro , Head of Business Development at WinGD Ltd. , recently argued that LNG’s role as shipping’s transitional fuel could last considerably longer than previously expected.

LNG has long been viewed as a bridge towards lower-carbon shipping. Current ordering patterns suggest that the transition window supported by that fuel may now extend much closer to 2050.

LNG accounts for more than 70% of alternative-fuel orders

According to Clarksons data reviewed by Xinde Marine News, global shipowners ordered 1,625 vessels totalling 43.57 million compensated gross tonnes during the first half of 2026.

Of these, approximately 246 vessels, representing 12.70 million CGT, were capable of operating on alternative fuels. They accounted for 15.1% of orders by vessel number and 29.1% by CGT.

LNG was by far the largest category.

A total of 173 LNG-capable vessels, representing 10.57 million CGT, were ordered during the six-month period. LNG therefore accounted for about 70.3% of alternative-fuel orders by vessel number and 83.3% by CGT.

The total included 54 LNG carriers, many of which use cargo boil-off gas as fuel. Even after excluding those ships, 119 non-LNG carriers were contracted with LNG propulsion.

Containerships accounted for 63 vessels and pure car and truck carriers for another 27. Together, those two segments represented around three-quarters of the non-LNG-carrier total. The remaining orders were distributed across product tankers, cruise ships, LNG bunker vessels, liquid CO₂ carriers, tankers, bulk carriers and tugboats.

DNV’s Alternative Fuels Insight platform uses a different methodology and records lower absolute numbers, but points to the same market trend. DNV counted 137 alternative-fuelled vessel orders in the first half of 2026, down from 155 a year earlier. LNG accounted for 73 of those orders, led by 42 containerships and 21 car carriers. Methanol accounted for only two vessels under the DNV methodology.

The difference between the Clarksons and DNV figures reflects variations in ship-type coverage, contract confirmation dates, treatment of gas carriers and definitions of alternative-fuel capability. Both datasets nevertheless show LNG retaining a substantial lead over the other main decarbonisation options.

Methanol’s slowdown began in 2025

Methanol’s loss of momentum has been particularly striking.

Clarksons recorded only four methanol-fuelled vessel orders during the first half of 2026, totalling 122,800 CGT and approximately 241,400 dwt.

They represented just 0.25% of all newbuild orders by vessel number and 0.28% by CGT.

The slowdown did not begin this year.

DNV recorded 61 methanol-fuelled vessel orders in 2025, down from 149 in 2024, a decline of around 59%. LNG remained the leading alternative fuel last year, with 188 orders excluding LNG carriers and a 31% share of total gross tonnage ordered.

The latest figures indicate that methanol contracting has weakened further in 2026.

At the same time, Clarksons recorded 85 vessels with methanol-ready designs during the first half, representing approximately 2.32 million CGT. This suggests owners have not abandoned methanol altogether. Many are prepared to preserve the option of conversion while postponing the cost and commercial exposure associated with installing a complete dual-fuel system today.

A methanol-ready notation generally requires a much smaller investment than a fully operational methanol fuel-storage, supply and propulsion system. It allows an owner to reserve space, structural arrangements and conversion pathways without immediately committing to a fuel whose long-term pricing and low-carbon supply remain uncertain.

The movement from dual-fuel orders towards ready designs therefore signals continued interest combined with greater capital discipline.

Owners are recalculating the cost of waiting

The regulatory backdrop is central to this shift.

IMO’s Net-Zero Framework was approved in draft form at MEPC 83 in April 2025, but the extraordinary session convened to adopt it was adjourned in October 2025. Discussions resumed at MEPC 84 in April and May 2026, with IMO currently scheduled to reconvene the extraordinary session on 4 December 2026, subject to confirmation by MEPC 85. Important details covering implementation, emissions pricing and fuel lifecycle treatment remain under negotiation.

This uncertainty has direct consequences for newbuilding investment.

A large merchant ship ordered today and delivered in 2028 or 2029 could remain in service well beyond 2050. Owners must make decisions now based on assumptions about fuel supply, bunkering networks, carbon prices, emissions intensity and retrofit potential over a period of more than two decades.

Moving too early into green methanol or ammonia could expose a vessel to a prolonged fuel-cost disadvantage if renewable production fails to expand quickly enough.

Remaining with conventional fuel oil creates a different risk. A conventionally fuelled ship may face rising costs under the EU Emissions Trading System, FuelEU Maritime and any future global greenhouse gas pricing mechanism.

LNG offers a more manageable intermediate position.

It already has an international production and distribution network, a growing bunkering system and extensive operational experience across multiple ship types. Its technical and commercial risks are better understood than those of most next-generation fuels.

WinGD says LNG typically trades at only a modest premium to very low sulphur fuel oil. Compared with conventional marine fuels, the company estimates that LNG can reduce onboard CO₂ emissions by 20% to 30%, NOx emissions by as much as 90% and SOx emissions by 99%.

As emissions acquire a direct financial cost, those reductions can translate into a measurable operating advantage.

WinGD sees a 5% to 6% OPEX advantage

WinGD’s modelling for typical containerships and bulk carriers indicates that LNG could deliver an operating expenditure saving of between 5% and 6% compared with VLSFO during the first eight years of a moderate global greenhouse gas pricing regime.

In that scenario, lower compliance expenses would more than offset LNG’s higher fuel price. The company also believes LNG remains competitive against other fuel options as emissions requirements become progressively more demanding towards 2050.

This helps explain why LNG continues to attract firm orders while many other fuel technologies remain prominent in announcements, pilot projects and long-term strategies but less visible in signed shipbuilding contracts.

For owners, the immediate question is increasingly focused on which propulsion platform can carry a vessel through the next 10 to 20 years of regulatory and fuel-market change at an acceptable cost.

The eventual zero-carbon fuel may remain unresolved. Investment decisions cannot be postponed indefinitely.

Bio-LNG and synthetic methane could extend the pathway

LNG’s long-term case depends partly on its ability to move beyond fossil natural gas.

An LNG-capable vessel can progressively introduce bio-LNG, also known as liquefied biomethane, and renewable synthetic methane into its fuel mix. These fuels have physical and chemical properties compatible with existing LNG storage, bunkering and engine systems.

WinGD says its low-pressure X-DF and high-pressure X-DF-HP engines can use bio-LNG and synthetic LNG in blends or as the sole fuel without hardware modifications. Its common engine platform also preserves the possibility of future conversion to methanol or ammonia if fuel economics change.

This gives owners a staged transition pathway.

A ship can initially operate on fossil LNG, increase the share of certified bio-LNG as supply grows and eventually move towards synthetic methane produced using renewable electricity. The carbon intensity of the vessel’s energy mix can therefore fall over time without replacing its principal fuel infrastructure.

Chain-of-custody and mass-balance systems could make that pathway more practical.

Under a recognised mass-balance arrangement, an owner could purchase certified low-carbon gas introduced elsewhere into an interconnected supply network and claim the corresponding emissions benefit without physically bunkering the same molecules into a particular vessel at a particular port.

IMO scheduled an expert workshop on fuel chain-of-custody models as part of its 2026 work programme, reflecting the importance of credible tracking and verification systems for future marine fuels.

For globally trading fleets, this could reduce dependence on a limited number of ports offering physical supplies of renewable methane.

LNG’s extended role still comes with conditions

Continued LNG ordering does not resolve the environmental debate surrounding the fuel.

Fossil LNG remains a carbon-based energy source. Its climate performance cannot be assessed solely through the CO₂ released during combustion. A full lifecycle calculation must also consider emissions from natural gas production, processing, liquefaction, transport and bunkering, as well as unburned methane released by engines.

Methane has a much stronger warming effect than CO₂ over shorter time horizons. High levels of methane slip from engines, combined with leakage across the upstream supply chain, can erode a significant part of LNG’s combustion-stage advantage.

The longevity of LNG as a credible transitional fuel therefore depends on continued reductions in methane slip, reliable lifecycle certification and a substantial expansion of competitively priced bio-LNG and synthetic methane.

Without progress in those areas, LNG may provide temporary compliance relief but struggle to support the deep emissions reductions required around 2050.

The transition is becoming more pragmatic

The first-half order data does not suggest that shipping has abandoned decarbonisation. It shows that owners are becoming more selective about how they pursue it.

LPG and ethane fuel orders have increased, although the growth is heavily concentrated among gas carriers able to consume part of their cargo as fuel. Ammonia remains in the early commercialisation phase. Hydrogen has yet to establish a viable deep-sea market. Methanol has entered a period of sharp retrenchment after several years of rapid contracting.

LNG, by comparison, combines proven engines, shipyard experience, established infrastructure and commercially available fuel. It can be deployed at scale today while retaining a pathway towards bio-LNG, synthetic methane and potentially other fuels through future conversion.

It may never become shipping’s universally accepted final fuel.

Under the current combination of regulatory uncertainty, limited green-fuel supply and high transition costs, however, LNG is increasingly being treated as the industry’s most practical transitional platform.

As Lazzaro observed, LNG was already expected to provide a bridge towards lower-carbon shipping.

The latest ordering data suggests that the industry may remain on that bridge for considerably longer than many had anticipated.

READ MORE

Technology

Technology

SunRui to Supply Rotor Sail Systems for Two 7,100DWT Self-Unloading Bulk Carriers

Technology

Technology

Complex cybersecurity threats demand practical solutions

Technology

Technology

Svanehoj acquires Henri Systems Holland, enhancing its tank gauging and aftermarket capabilities

Technology

Technology

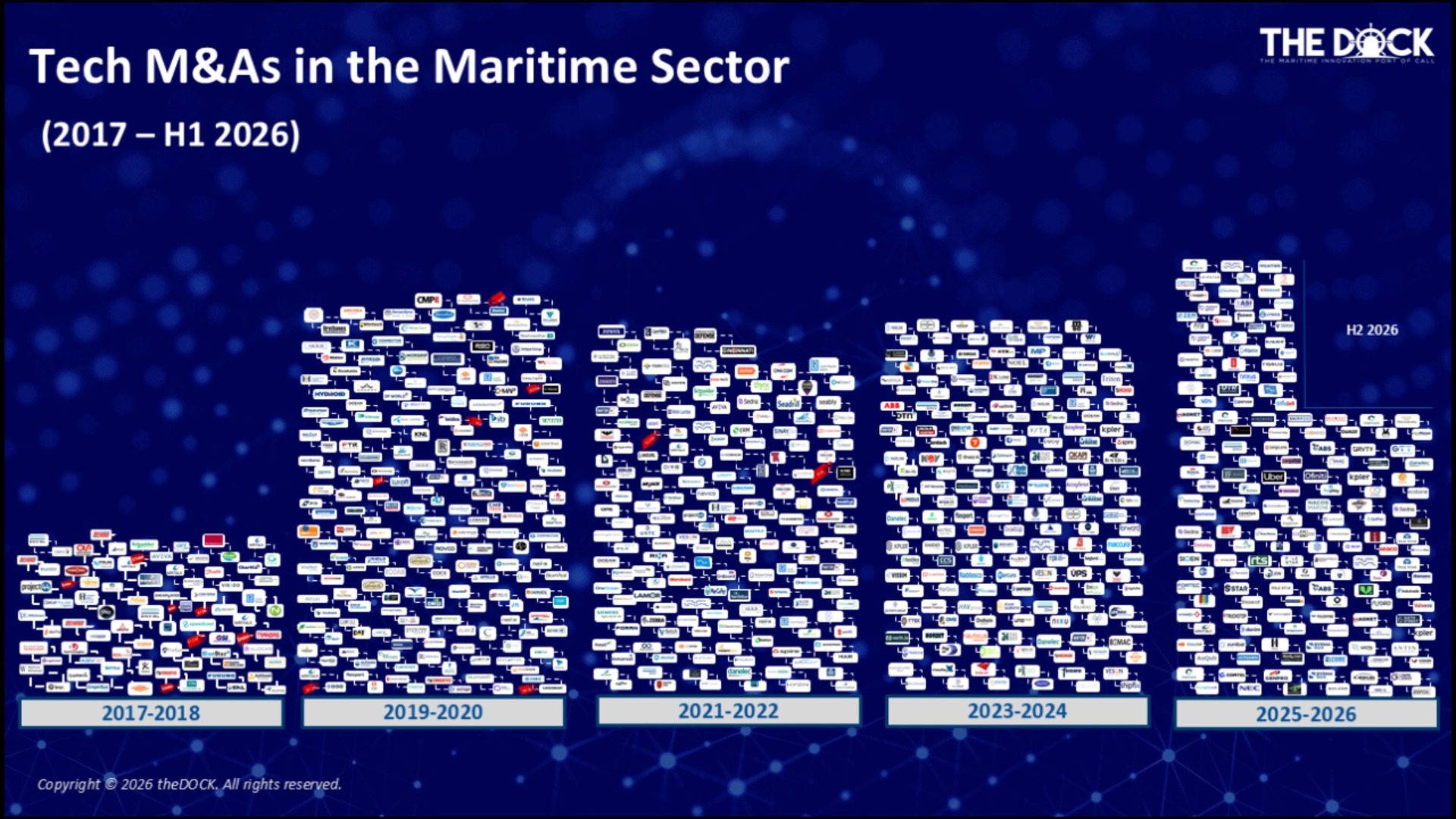

Maritime Tech Enters the Platform Era as M&A Activity Accelerates

Technology

Technology

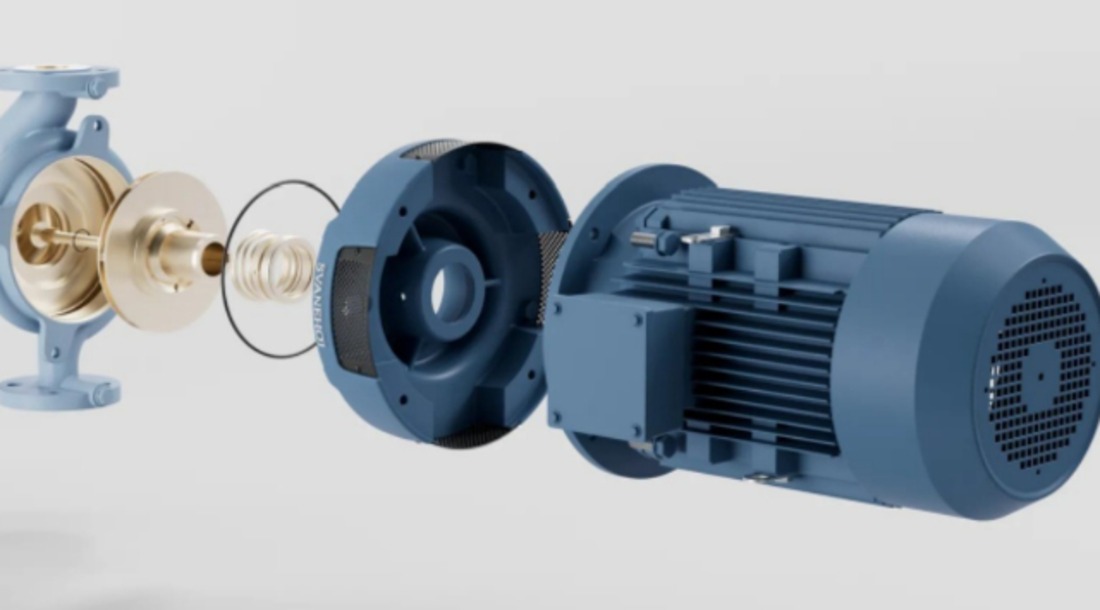

INNOVATION AT SEA: SVANEHØJ INTRODUCES NEXT-GEN SHIP ENGINE ROOM PUMPS

Technology

Technology

AI’s Boom Is Starting to Reshape Shipping’s Asset Logic

Technology

Technology

How Far Has AI Advanced in China’s Port and Shipping Sector?

Technology

Technology

GTT Redraws Its Strategic Map: From LNG Containment Specialist to a Dual-Engine Platform Built Around GTT Energy and GTT Marine

Technology

Technology

Is Headway becoming green shipping’s Doraemon?

Technology

Technology