Maritime Tech Enters the Platform Era as M&A Activity Accelerates

A decade of consolidation is reshaping the sector as shipping companies seek trusted data, cybersecurity and integrated decision-making tools

The maritime technology market is moving beyond its fragmented start-up phase and entering an era increasingly dominated by larger, multi-application platforms.

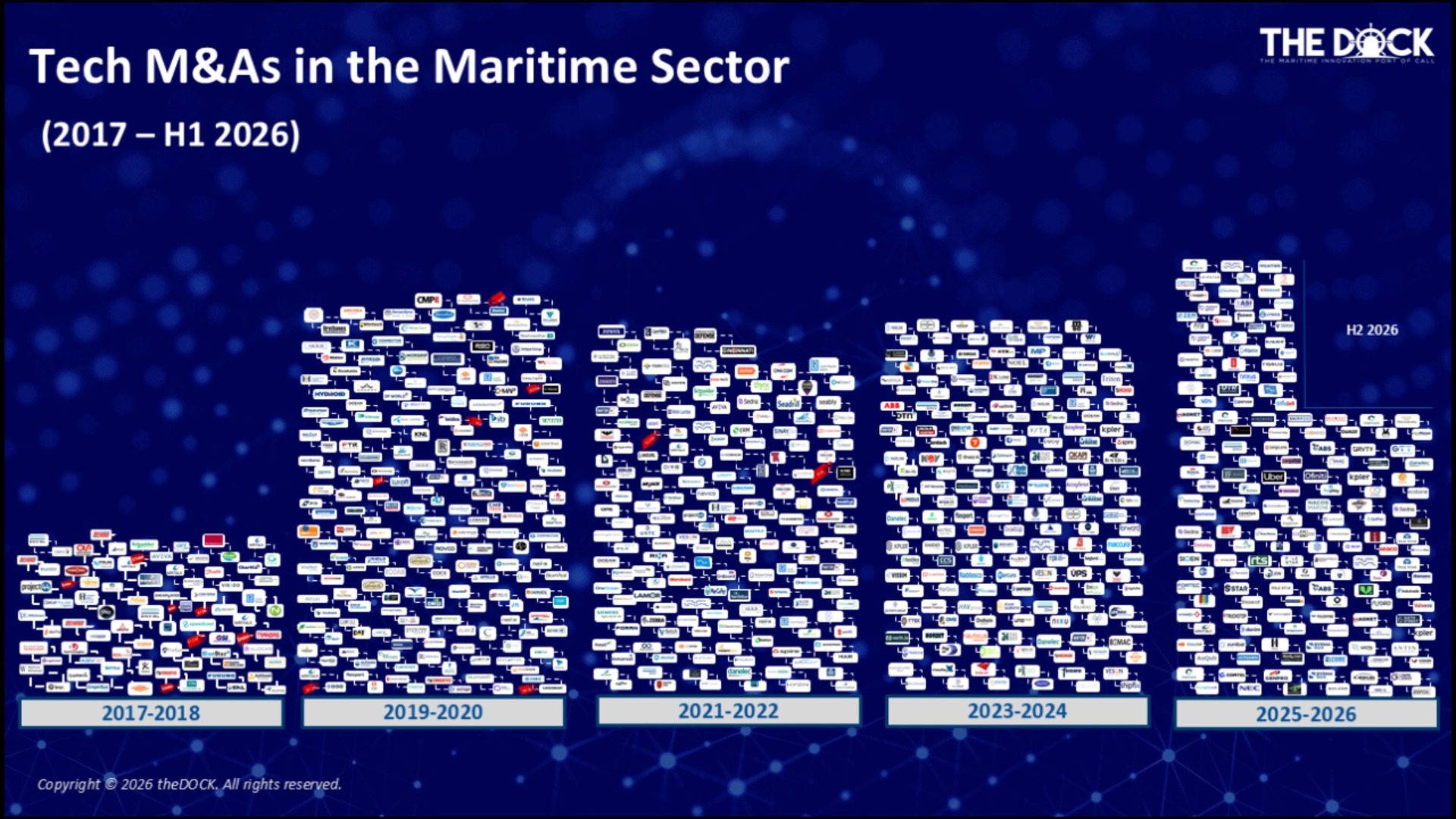

According to an analysis published by Hannan Carmeli of theDOCK on 9 July 2026, the sector has recorded 381 transactions since 2017, with merger and acquisition activity continuing to accelerate.

Only eight maritime technology deals were recorded in 2017. By 2025, the annual total had risen to a record 52 transactions. Based on the pace maintained during the first half of 2026, Carmeli projects that the combined 2025–2026 cycle could exceed 100 deals, the highest two-year total covered by the study.

One of the clearest examples of this consolidation came in January 2026, when Signal Ocean, part of The Signal Group, acquired AXSMarine.

The deal brought AXSMarine’s established shipping intelligence products—including AXSDry, AXSTanker and Alphaliner—into the same group as Signal Ocean’s data analytics and artificial intelligence capabilities.

Although the financial terms were not disclosed, the transaction became one of the most closely watched maritime technology acquisitions announced at the beginning of 2026. It also illustrated a broader change in the market: buyers are no longer seeking isolated software tools alone. They are increasingly assembling platforms capable of connecting data, market intelligence and operational workflows.

From digital efficiency to operational resilience

The first wave of maritime digitalisation was largely driven by efficiency.

Shipowners, charterers and managers wanted to automate repetitive work, improve fleet performance and reduce operating costs. Technology was often purchased to solve a specific problem within one department.

That rationale has expanded significantly.

Since 2020, shipping companies have faced repeated supply chain disruption, port congestion, sanctions, geopolitical conflicts and changes in global commodity flows. The Red Sea crisis, which escalated from late 2023, further altered sailing distances, fleet availability, insurance costs and voyage economics.

These events have shown that technology is no longer simply an efficiency tool. It has become part of operational resilience and risk management.

Shipping companies increasingly need to understand not only where vessels and cargoes are located, but also how security incidents, sanctions, political decisions and chokepoint disruption could affect their operations.

In this environment, the industry does not merely need more data. It needs information that is timely, verifiable and trusted.

Poor-quality information can result in a mispriced voyage, a missed fixture, an avoidable compliance risk or a vessel being positioned in the wrong market.

This helps explain why established maritime intelligence providers have become attractive acquisition targets. Their value lies not only in software, but also in proprietary datasets, industry expertise, customer relationships and the trust built over many years.

Vessel operations lead the acquisition market

Carmeli’s analysis shows that vessel operations and autonomous shipping have been the largest category of maritime technology M&A since 2017, accounting for more than one-third of all transactions.

The category includes predictive maintenance, navigation technology, fleet performance systems, remote monitoring and the early development of autonomous vessel operations.

The number of transactions reflects shipping’s continuing investment in smarter fleets. It also highlights the fragmented nature of existing maritime technology.

Many companies still operate multiple systems that do not communicate effectively with one another. Commercial, technical, operational and compliance teams may work from separate databases and different versions of the same information.

The opportunity for buyers is therefore not simply to acquire more applications, but to connect them.

Supply chain platforms gain importance

Supply chain and logistics technology has been the second most active acquisition category identified by theDOCK.

Its share has increased as buyers attempt to connect maritime transport with port operations, cargo management and inland logistics.

This reflects the changing expectations of customers.

A standalone application may perform one function effectively, but shipping companies increasingly want platforms that can connect vessel scheduling, voyage execution, freight analysis, cargo tracking and port activity.

The objective is to create a more integrated decision-making environment and reduce dependence on disconnected legacy systems.

The Signal Ocean–AXSMarine transaction fits this trend. Its strategic value lies in the potential to combine shipping market intelligence, freight analytics and commercial workflows within a broader technology ecosystem.

Cybersecurity becomes a strategic priority

Cybersecurity and maritime safety have also grown rapidly as acquisition categories.

According to Carmeli, they represented less than 9% of transactions across the full study period, but their share almost doubled during 2023–2026.

This increase is closely connected to digitalisation.

As vessels, ports and shore-based systems become more interconnected, the consequences of cyber incidents become more serious. Attacks can affect commercial information, cargo operations, navigation systems and critical maritime infrastructure.

Buyers are therefore looking for technology that can provide secure data access, threat detection, business continuity and reliable governance, rather than efficiency alone.

For shipping companies, confidence in a platform increasingly depends on whether it can protect the information and workflows placed inside it.

Sustainability technology remains active

Sustainability-related transactions have also remained resilient.

The introduction of the European Union Emissions Trading System for shipping from 2024 and FuelEU Maritime from 2025 increased demand for emissions measurement, regulatory reporting, voyage optimisation and fuel-related decision tools.

Environmental performance is becoming increasingly connected to chartering, financing and asset valuation.

As a result, sustainability software is moving from the margins of corporate reporting into the centre of daily commercial and operational decision-making.

Private equity accelerates consolidation

Corporate buyers have accounted for most maritime technology acquisitions over the past decade, but private equity has become more influential during the latest cycle.

The importance of private equity lies not only in the amount of capital available. PE-backed companies are often built as consolidation platforms, with mandates to acquire complementary businesses and create scale across several applications.

Carmeli highlights Veson Nautical, Kpler and Marcura as examples of maritime technology platforms supported by major private-equity investors.

These companies can use acquisitions to expand their product portfolios, enter adjacent market segments and deepen relationships with existing customers.

This creates a different consolidation dynamic from that of traditional corporate acquisitions. PE-backed platforms often move faster and pursue scale more systematically, increasing competition for established maritime software and data businesses.

The rise of the one-stop platform

The direction of the market is becoming clear.

Customers increasingly want platforms that bring together trusted data, market intelligence and operational tools. They want fewer disconnected systems and a more consistent view across commercial, technical and compliance functions.

A one-stop maritime technology platform does not necessarily need to own every application. It must, however, allow information to move securely and efficiently across different workflows.

For customers, this can reduce implementation costs, simplify system management and support faster decisions.

For technology providers, the platform model creates recurring revenue, stronger customer retention and access to larger pools of proprietary data.

There are also risks.

Further consolidation could reduce competition and increase dependence on a limited number of technology providers. Integrating acquired systems, datasets and corporate cultures may also prove difficult.

Shipping companies will therefore need to assess data ownership, interoperability, cybersecurity and service continuity before placing critical functions with a single provider.

A market built around trust

Maritime technology M&A is likely to remain active because the structural drivers behind it have not disappeared.

The supplier landscape remains fragmented. Regulatory requirements are becoming more complex. Shipping companies are under pressure to digitalise, while proprietary data is becoming increasingly valuable.

Geopolitical uncertainty may change routes, costs and trading patterns, but the need for trusted information and secure systems is permanent.

The platforms now being assembled are likely to define the maritime technology landscape for the decade ahead.

Independent companies will continue to have opportunities, particularly where they possess distinctive data, specialist maritime knowledge or technology that solves a critical problem.

However, the space for narrowly focused providers without a clear role in a broader ecosystem may continue to narrow.

The next phase of maritime technology competition will therefore be determined not only by who has the best individual application, but by who can build the most trusted, secure and comprehensive platform.

READ MORE

Technology

Technology

SunRui to Supply Rotor Sail Systems for Two 7,100DWT Self-Unloading Bulk Carriers

Technology

Technology

Complex cybersecurity threats demand practical solutions

Technology

Technology

Svanehoj acquires Henri Systems Holland, enhancing its tank gauging and aftermarket capabilities

Technology

Technology

Methanol Orders Stall as LNG’s Transition Window Looks Set to Run Longer

Technology

Technology

INNOVATION AT SEA: SVANEHØJ INTRODUCES NEXT-GEN SHIP ENGINE ROOM PUMPS

Technology

Technology

AI’s Boom Is Starting to Reshape Shipping’s Asset Logic

Technology

Technology

How Far Has AI Advanced in China’s Port and Shipping Sector?

Technology

Technology

GTT Redraws Its Strategic Map: From LNG Containment Specialist to a Dual-Engine Platform Built Around GTT Energy and GTT Marine

Technology

Technology

Is Headway becoming green shipping’s Doraemon?

Technology

Technology