Hormuz Fallout Fuels One of Container Shipping’s Biggest Rate Spikes in History

Aftershocks of the Strait of Hormuz “Chokehold” Emerge: Container Freight Rates Are Seeing a Rare Historic Surge

Xinde Marine News reports that the impact of the Strait of Hormuz crisis on global shipping markets is now spreading beyond tankers, LNG and energy prices, and is increasingly being transmitted into the container shipping market.

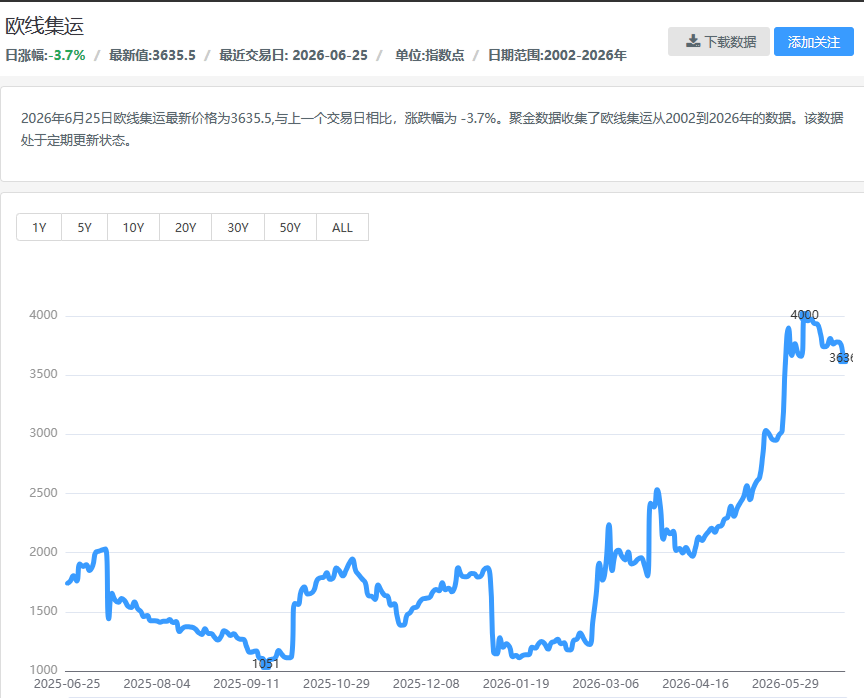

On July 2, Drewry’s World Container Index (WCI) rose 9% week-on-week to USD 4,530 per 40-foot container. Drewry said the latest increase was mainly driven by rising freight rates on the transpacific and Asia-Europe routes, with spot rates continuing to move higher. Specifically, rates from Shanghai to New York increased 11% to USD 7,902 per 40-foot container, while Shanghai to Los Angeles rose 10% to USD 6,349. Shanghai to Genoa climbed 10% to USD 6,360, and Shanghai to Rotterdam increased 7% to USD 4,682. Drewry expects rates to rise further in the coming weeks.

This has brought renewed attention to one market view: the Strait of Hormuz crisis is creating another major rate spike in the history of container shipping. U.S. maritime historian Sal Mercogliano commented on social media that this is the third-largest surge in container freight rates in history, following the pandemic-era rate boom and the Red Sea crisis-driven rerouting spike. He added that the current increase could even move closer to becoming the second-largest.

Xeneta’s data supports this view. As of June 25, spot rates from the Far East to the U.S. West Coast had risen to USD 5,909 per 40-foot container, while Far East to the U.S. East Coast reached USD 7,313. Far East to North Europe stood at USD 4,763, and Far East to the Mediterranean reached USD 6,044. Compared with the pre-crisis level at the end of February, rates from the Far East to the U.S. West Coast were up 214%, Far East to the U.S. East Coast up 176%, Far East to North Europe up 115%, and Far East to the Mediterranean up 82%. Over the past month alone, rates on the Far East–U.S. West Coast, U.S. East Coast, North Europe and Mediterranean routes increased by 81%, 67%, 65% and 40%, respectively.

The Strait of Hormuz itself is not a core corridor for the world’s main container shipping routes. Freightos previously noted that the strait normally carries about 20% of global oil flows, but only around 2% to 3% of global container volumes. By comparison, the Red Sea typically handles around 20% of global container traffic. For this reason, at the early stage of the crisis, the market generally believed the direct impact on container shipping would be limited.

However, subsequent market movements show that Hormuz’s impact on container shipping does not depend solely on the proportion of container vessels directly transiting the strait. The real transmission channels are mainly threefold: rising bunker costs, disruption to Gulf service networks, and carriers’ continued push for higher FAK rates, GRIs and PSS charges amid the early peak season and tight capacity.

READ MORE

Containers

Containers

COSCO SHIPPING Adds Another Full-Electric Container Vessel

Containers

Containers

Maersk Lifts 2026 Guidance by Up to $3.5bn as Container Market Turns More Profitable

Containers

Containers

Ningbo Containerized Freight Index Weekly Commentary: Freight Rate Trends Continued to Diverge; Composite Index Maintained Upward Trend

Containers

Containers

From 96 Containers to a Three-Storey Office Building in Just 11 Days

Containers

Containers

China-Europe Cargo Gets an Arctic Shortcut as Sea Legend Resumes Weekly Service

Containers

Containers

MPCC Buys Four 7,000 TEU Ships for USD 340m as Mid-Sized Container Tonnage Heats Up

Containers

Containers

Ningbo Containerized Freight Index Weekly Commentary Freight Rate Trends Diverged Across Routes; Composite Index Edged Up

Containers

Containers

European Route Freight Rates Enter a "Stepped Consolidation Phase"; Mid-July Rate Increase Window Remains Open

Containers

Containers