MPCC Buys Four 7,000 TEU Ships for USD 340m as Mid-Sized Container Tonnage Heats Up

Xinde Marine News — Oslo-listed tonnage provider MPC Container Ships ASA is pushing its fleet renewal strategy into a larger vessel segment.

On 25 June, MPCC announced that it had agreed to acquire four 2023–2024 built 7,000 TEU eco-design conventional-fuel container vessels from an unrelated third party. Each vessel is secured with a three-year fixed-rate time charter to a top-five liner company.

The total acquisition price is USD 340 million, equivalent to around USD 85 million per vessel. According to MPCC, the charters attached to the vessels are expected to generate approximately USD 180 million in revenue and USD 140 million in EBITDA over the three-year charter period. Delivery of the vessels is expected in October and November 2026, subject to inspection and customary closing conditions.

The deal is more than a simple fleet expansion. MPCC is acquiring young, efficient, charter-backed mid-sized vessels, while also fixing forward employment for existing tonnage, selling older non-core assets and securing long-term financing for its newbuilding programme.

It is a transaction that underlines a broader shift in the container shipping asset market: modern mid-sized containerships are once again attracting strong attention from shipowners, liner operators and shipping banks.

MPCC moves up into the 7,000 TEU segment

MPCC has long been known as an independent tonnage provider focused on feeder and small-to-mid-sized container vessels. Its core business model is to own containerships and charter them out to liner companies on fixed-rate contracts, serving intra-regional and regional-to-regional trades.

The acquisition of four 7,000 TEU vessels therefore marks a meaningful step up in vessel size for the company.

According to Xinde Marine News’ understanding, MPCC’s largest existing vessels before this deal were two 5,500 TEU ships built in 2022. Once the acquisition is completed, MPCC will formally enter the 7,000 TEU segment, expanding its platform from traditional feeder and smaller mid-sized vessels into a broader mid-sized containership category.

The 7,000 TEU class occupies a highly relevant position in today’s liner network.

These vessels are flexible enough to serve intra-Asia, Asia–Middle East, Asia–Indian Subcontinent, Asia–Africa and north-south trades, while also being able to support certain mainline and regional transshipment networks. Compared with ultra-large containerships, they require less cargo concentration and are less dependent on deep-water hub ports. Compared with smaller feeder vessels, they offer stronger unit-cost efficiency and greater network reach.

MPCC CEO Constantin S. Baack said in the company’s announcement that global container shipping is undergoing a structural shift toward intra-regional trade, with feeder vessels and the mid-sized segment up to 10,000 TEU set to benefit disproportionately. He noted that modern, fuel-efficient tonnage in this size class remains undersupplied, while versatile vessels deployable across almost any trade lane are becoming the natural successors to ageing classic Panamax and first-generation post-Panamax ships.

That statement captures the core logic behind this transaction. The 7,000 TEU segment is becoming increasingly important in the renewal cycle of regional supply chains, liner network redesign and the replacement of older Panamax and post-Panamax tonnage.

A deal that echoes MPCC’s earlier interview with Xinde Marine News

The acquisition closely matches the market view Baack shared in a recent interview with Xinde Marine News.

In that interview, Baack said regional markets and inter-regional connectivity would become increasingly important over the next five to ten years. Over the past two decades, the growth of east-west mainline trades was largely driven by Chinese exports and consumer demand in Europe and North America. In the years ahead, trade connections between Southeast Asia, the Far East and other emerging markets are expected to play a larger role in container shipping demand.

This helps explain why MPCC is now willing to move beyond its traditional feeder focus and acquire 7,000 TEU vessels.

Ships of around 7,000 TEU combine economies of scale with network flexibility. They can serve intra-regional routes, regional-to-regional trades and flexible deployment needs when liner companies adjust their networks. For carriers redesigning regional and inter-regional services, these vessels offer a wider range of use cases than many larger or smaller vessel classes.

Baack also stressed in the interview that capacity discussions should not be based solely on total containership fleet numbers. While the pressure from large-vessel orderbooks is more visible, the smaller and mid-sized segments have their own supply-demand logic. Regional trades require flexible tonnage, demolition has remained limited in recent years, and a significant portion of the small and mid-sized fleet is ageing. Around a quarter of the fleet in these segments is already over 20 years old. At the same time, vessel efficiency has become directly linked to operating cost, not just emissions performance.

That background explains the profile of the assets MPCC is buying. The four ships were built in 2023 and 2024, are young and fuel-efficient, and come with three years of fixed-rate charter coverage. For MPCC, these assets provide immediate cash flow and should still retain strong re-chartering potential when the current employment expires.

The real shortage is available tonnage

One of Baack’s key observations in the Xinde Marine News interview was that the crucial issue in today’s charter market is not simply the total fleet size, but the number of vessels actually available.

He noted that ten years ago, many container vessels were fixed for three, six or twelve months. Today, more ships are being locked into two- or three-year charters. In the past, roughly 1,500 containerships could enter the charter market each year. That number has now dropped to around 400.

This means that even when spot freight rates ease, the charter market may not move in the same way. Liner companies that need modern tonnage for the next one to two years must act earlier. Discussions that once started 30 days before a vessel became open are now taking place several quarters ahead.

MPCC’s acquisition of four 7,000 TEU vessels with three-year charters fits directly into this market dynamic. The buyer secures predictable cash flow, the charterer secures future vessel availability, and lenders see a clear earnings base behind the transaction.

In practical terms, MPCC is not buying bare vessel exposure. It is acquiring a package of young tonnage, top-tier charterer employment, three-year cash flow and future residual value optionality. That combination gives the assets stronger financial characteristics and makes them more bankable.

USD 85m per vessel

At USD 340 million in total, the acquisition price works out at around USD 85 million per vessel.

That is not a low price. But the vessels are very young, built in 2023 and 2024, and are available far sooner than equivalent newbuildings. For the buyer, the transaction saves two to three years of waiting time and immediately provides charter-backed earnings. Compared with older secondhand tonnage, these vessels also command a premium because of their fuel efficiency, regulatory profile, charterer acceptance and remaining economic life.

The three-year fixed-rate charters are the critical part of the transaction. MPCC expects the four vessels to generate around USD 180 million in revenue and USD 140 million in EBITDA during the charter period. That means a substantial portion of the purchase price is supported by contracted earnings.

At the end of the three-year period, the vessels will still be only five to six years old. They should remain attractive to major liner operators and retain multiple options for re-chartering, extension or potential asset sale.

This is the logic behind MPCC’s reference to de-risking residual value. The first three years of cash flow reduce the asset risk, while the company retains upside after the charters expire.

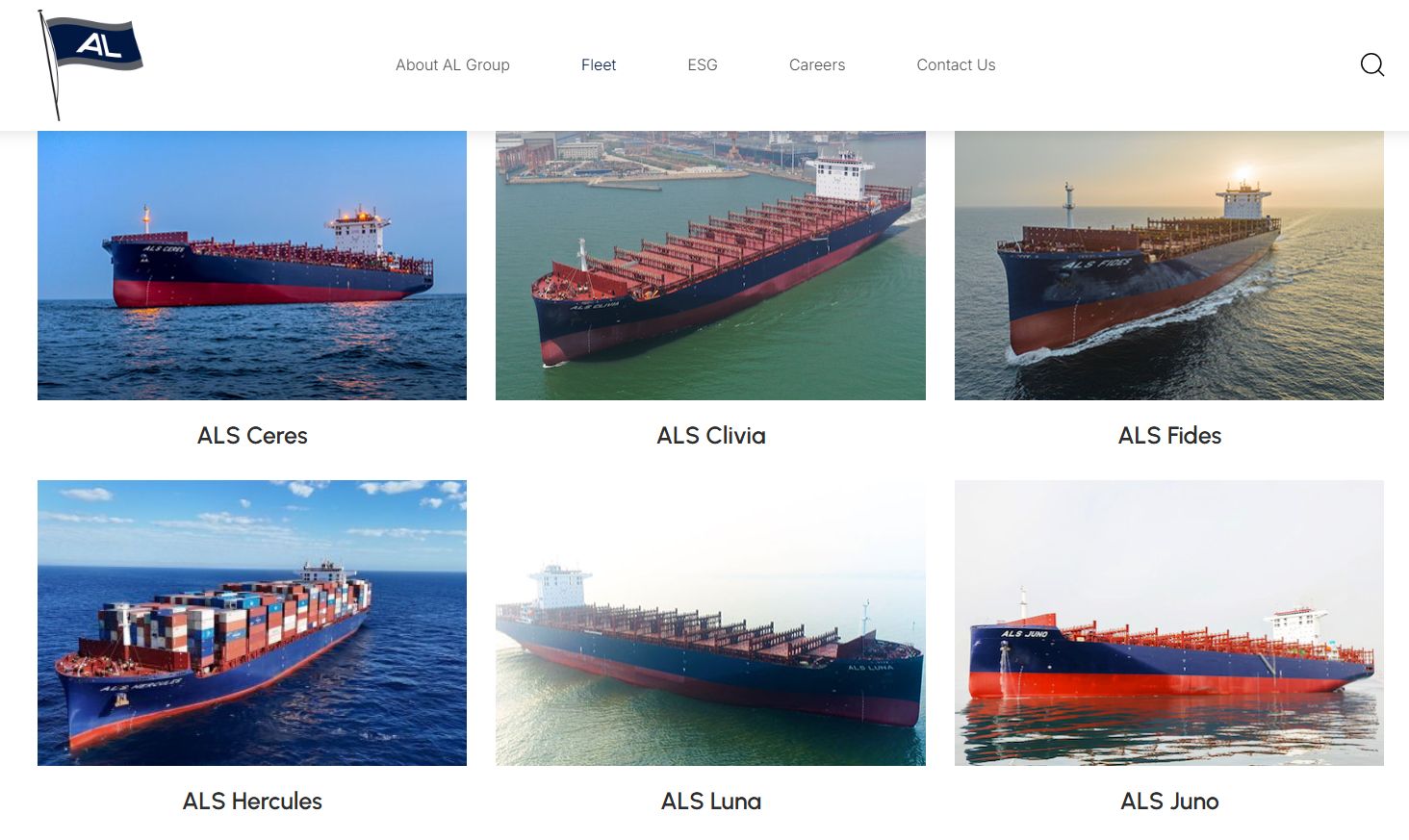

Who is the seller? Market clues point to AL Group’s 7,111 TEU series

MPCC has not disclosed the seller or the names of the vessels. The company only described the seller as “an unrelated third party”.

However, based on publicly available fleet information and vessel specifications, market clues point strongly toward AL Group, the Asiatic Lloyd / Atlantic Lloyd / Bunnemann Group platform, and its 7,111 TEU series.

AL Group’s fleet list includes six 7,111 TEU container vessels built by DSIC in 2023 and 2024: ALS Ceres, ALS Clivia, ALS Fides, ALS Hercules, ALS Luna and ALS Juno. Their size, age, builder and design profile appear to match MPCC’s description of 2023–2024 built 7,000 TEU eco-conventional vessels.

China State Shipbuilding Corporation previously disclosed that AL Maritime Holding, a company within the AL Group structure, had ordered six 7,100 TEU container vessels at DSIC. The ships were designed by Shanghai Merchant Ship Design & Research Institute, with an overall length of around 255 metres and a beam of 42.8 metres. They were designed to meet IMO Tier III requirements and EEDI Phase III standards.

TradeWinds has also previously reported that ALS Ceres and its five sister vessels were chartered to CMA CGM. CMA CGM is one of the world’s top five liner companies, which matches MPCC’s description that the vessels are chartered to a top-five carrier.

A reasonable market inference is therefore that the four 7,000 TEU vessels being acquired by MPCC may come from AL Group’s six-ship 7,111 TEU series. If this inference is correct, the charterer is likely CMA CGM.

That said, MPCC, AL Group and CMA CGM have not formally confirmed the vessel names or counterparties. Until official confirmation emerges, this should remain a market-based assessment rather than a confirmed fact.

Buying young ships, selling older assets

MPCC also announced forward chartering and sale activity alongside the acquisition.

The company has fixed AS Pamela and AS Anne on new charter contracts. AS Pamela has been fixed for 24 to 27 months, while AS Anne has been fixed for 30 to 32 months. The contracts were concluded around six to nine months forward on average and will commence in the second quarter of 2027 and the fourth quarter of 2026 respectively.

MPCC has also agreed to sell AS Selina for USD 24 million. Handover is expected after expiry of the current charter, scheduled between the end of the fourth quarter of 2026 and the beginning of the first quarter of 2027. Separately, MPCC has agreed to sell AS Angelina for USD 17 million. The vessel is approaching its 20-year class renewal in 2027, and handover is expected during the third quarter of 2026.

This buying and selling pattern shows a clear fleet renewal logic. MPCC is replacing older, less strategic tonnage with younger, more efficient and charter-backed vessels.

That strategy is increasingly relevant in the small and mid-sized container vessel market. Regional trade, transshipment demand and rerouting-related capacity absorption continue to support the charter market. At the same time, older vessels face rising maintenance, special survey, energy efficiency and compliance costs. Selling non-core vessels before major class renewal can release capital and reduce future ageing-related exposure.

Disciplined expansion backed by customers and cash flow

The transaction also reflects one of the principles Baack emphasised in his interview with Xinde Marine News: MPCC does not aim to grow simply for the sake of scale.

Baack said timing matters in shipping cycles, but long-term resilience depends on execution capability, customer relationships, risk control and balance sheet discipline. MPCC grew from zero to more than 60 vessels in around 18 months during an earlier market window because it was able to execute quickly. Today, its newbuilding and secondhand investment strategy is more focused on customer support and earnings visibility.

The latest transaction follows that logic closely. MPCC is buying young ships, but every vessel comes with a three-year fixed-rate charter. The company is selling non-core older vessels, reducing fleet age, and has secured a USD 375 million long-term loan to support its newbuilding programme.

This is not an isolated asset purchase. It is part of a coordinated approach built around fleet renewal, customer demand, financing discipline and future cash flow visibility.

USD 375m financing supports the newbuilding programme

Another important part of the announcement is MPCC’s USD 375 million senior secured term loan.

The facility was fully underwritten by Société Générale. The final lending group includes BNP Paribas, Crédit Agricole, ING and KfW IPEX-Bank. The loan will support ten of MPCC’s 16 newbuildings ordered last year and has a ten-year tenor from delivery.

MPCC also said that a further USD 75 million facility related to two 4,500 TEU newbuildings has received credit approval and is expected to close in the second half of 2026.

This indicates that MPCC’s fleet renewal programme has moved firmly into the funding stage. Over the past year, the company has placed newbuilding orders across several vessel sizes, including 1,600 TEU, 3,700 TEU and 4,500 TEU ships. The USD 375 million loan provides funding support for ten of those newbuildings and reduces future delivery-period financing pressure.

MPCC also noted that it currently has 30 debt-free vessels and significant undrawn capacity under its revolving credit facility. For an independent tonnage provider, the alignment between financing cost, leverage, charter duration and delivery schedule is critical. The support of major European shipping banks indicates lender confidence in MPCC’s contract coverage, asset quality and fleet renewal strategy.

Contract coverage rises further

The acquisition, chartering and financing initiatives also improve MPCC’s earnings visibility.

Following these developments, MPCC’s contracted revenue backlog will rise to USD 2.2 billion. Charter coverage will stand at 99% for 2026, 74% for 2027 and 48% for 2028.

The company has also revised its 2026 guidance upward. Revenue is now expected at USD 460 million to USD 470 million, compared with the previous range of USD 450 million to USD 460 million. EBITDA guidance has been increased to USD 280 million to USD 300 million, from USD 260 million to USD 280 million.

These figures show that MPCC is continuing to lock in a high proportion of its earnings for the next two to three years. For a listed tonnage provider, contracted revenue visibility supports dividends, financing capacity and continued fleet renewal. It also reduces sensitivity to short-term market volatility.

MPCC’s strategy is not to place the entire fleet on spot exposure. Instead, the company is locking in part of its future earnings when the charter market is attractive, while retaining re-pricing potential through selected vessels and future open positions.

Mid-sized containerships are being repriced

The broader significance of this deal lies in the repricing of mid-sized containership assets.

Over the past several years, the containership newbuilding market has been dominated by very large vessels and dual-fuel mainline ships. Liner companies have invested heavily in 24,000 TEU, 16,000 TEU and 13,000 TEU classes to reduce unit costs and prepare for future alternative fuel and emissions requirements.

Yet in real liner networks, vessels of around 7,000 TEU continue to play an essential role.

Global trade is becoming more regionalised. Southeast Asia, India, the Middle East, Latin America and Africa are all reshaping container demand patterns. Disruptions around the Red Sea, the Panama Canal and the Strait of Hormuz have also pushed liner companies to value network flexibility and routing optionality more highly. Mid-sized vessels can shift between regions and support both mainline and regional networks.

At the same time, older classic Panamax and first-generation post-Panamax vessels are entering a replacement phase. Many of these ships are ageing, less efficient and less attractive to major liner companies. If newbuilding supply continues to focus heavily on larger ships and specific alternative-fuel designs, modern mid-sized tonnage may remain scarce.

MPCC’s willingness to pay around USD 85 million per vessel for young, charter-backed 7,000 TEU tonnage reflects this asset logic. The market is increasingly valuing modern, fuel-efficient, flexible and charter-supported mid-sized containerships as scarce assets.

A boundary expansion for MPCC

MPCC’s traditional identity has been clear: feeder shipowner, small-to-mid-sized containership tonnage provider and regional trade specialist.

After this deal, that identity will broaden. MPCC will remain focused on the small-to-mid-sized market, but its asset boundary will extend into the 7,000 TEU class. This gives the company a wider range of cooperation with major liner companies and more flexibility in future portfolio construction.

MPCC said the acquisition strengthens its ability to serve top-tier global liner companies across a wider range of vessel sizes. For a tonnage provider, vessel diversity matters. A broader vessel range creates more matching opportunities with liner networks, charterer requirements and regional trade growth.

The 7,000 TEU class may now become a new reference point in MPCC’s fleet renewal strategy. Whether the company expands further in this segment will depend on the availability of suitable young assets, liner companies’ willingness to commit to medium- or long-term charters, and MPCC’s ability to maintain a sufficient margin of safety between asset price, charter duration and financing cost.

Conclusion

MPCC’s USD 340 million acquisition of four 7,000 TEU vessels is a classic window-of-opportunity transaction. The buyer gains young tonnage, three years of fixed-rate employment and strong cash flow visibility. If the seller is indeed AL Group, it would be realising value on recently delivered assets. The charterer, likely CMA CGM based on market clues, continues to secure modern mid-sized tonnage for its regional and inter-regional network needs.

The transaction sends a wider signal to the market. Beyond ultra-large container vessels and green dual-fuel newbuildings, 7,000 TEU-class ships are moving back into focus.

As regional trade grows, liner networks are redesigned, older tonnage is replaced and environmental compliance pressures rise, modern mid-sized containerships may become increasingly scarce. MPCC’s latest move is therefore more than a secondhand vessel purchase. It is an early bet on the long-term value of flexible, efficient mid-sized container tonnage.

READ MORE

Containers

Containers

European Route Freight Rates Enter a "Stepped Consolidation Phase"; Mid-July Rate Increase Window Remains Open

Containers

Containers

Container Freight Rates Surge as SCFI Nears 3,000 Points

Containers

Containers