Container Freight Rates Surge as SCFI Nears 3,000 Points

Xinde Marine News — Global container freight rates are rising sharply again, with the Shanghai Containerized Freight Index (SCFI) approaching the 3,000-point mark.

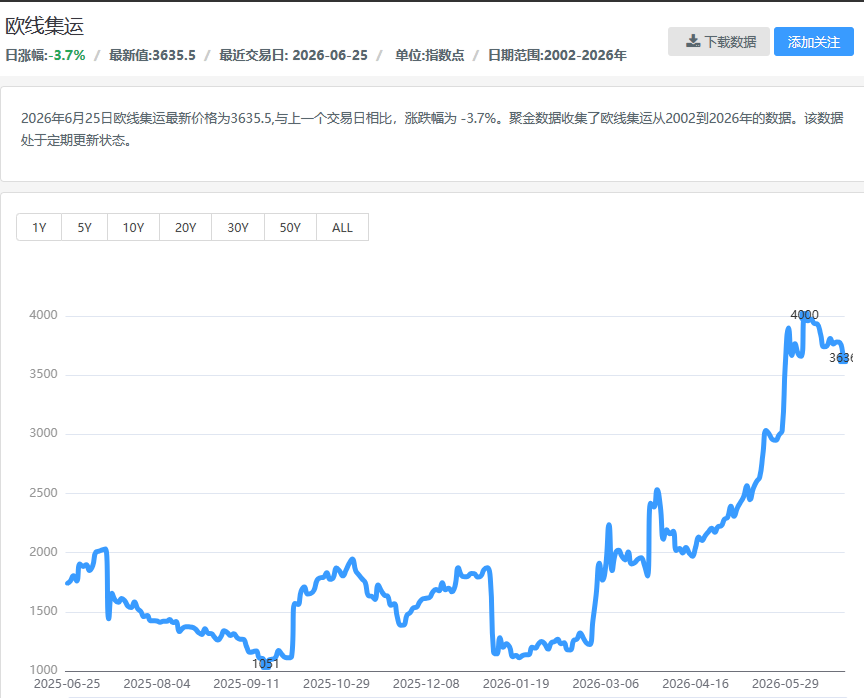

According to the latest data from the Shanghai Shipping Exchange, the SCFI reached 2,985.22 points on June 12, up 258.74 points from the previous week. This represents a weekly increase of about 9.49%.

It was the seventh consecutive weekly rise for the index. On April 24, the SCFI stood at 1,875.26 points. By June 12, it had climbed to 2,985.22 points. In less than two months, the index rose by 1,109.96 points, or about 59.2%.

Major trade lanes rise together

The latest SCFI data shows that freight rates rose across major trade lanes.

Rates from the Far East to the US West Coast reached USD 5,101 per FEU, up USD 549 from the previous week. Rates to the US East Coast reached USD 6,321 per FEU, up USD 580.

Europe-bound rates also increased strongly. Rates from the Far East to North Europe reached USD 3,064 per TEU, up USD 459, while rates to the Mediterranean reached USD 4,172 per TEU, up USD 340.

Drewry’s latest World Container Index showed a similar trend. For the week of June 11, the WCI rose 3% to USD 3,549 per 40ft container. Shanghai–New York rose 7% to USD 5,870 per 40ft container, while Shanghai–Los Angeles rose 3% to USD 4,683. Shanghai–Rotterdam rose 5% to USD 3,768, and Shanghai–Genoa rose 1% to USD 5,139.

The rise is no longer limited to one route. Transpacific, Asia–Europe and Mediterranean trades are all moving higher.

World Cup demand supports the US routes

The US routes remain among the strongest parts of the market.

One special factor this year is the 2026 FIFA World Cup, which started on June 11 and is being held across the United States, Canada and Mexico.

For North America, the World Cup is not only a sports event. It is also a major consumer and retail event. Jerseys, scarves, hats, flags, souvenirs, display materials, promotional goods, food and beverage supplies, hotel items and event-related products all need to arrive before the tournament.

Because ocean shipping takes time, many of these goods had to be shipped weeks or months in advance. A large part of this supply chain still comes from Asia, which supports container demand from the Far East to both the US West Coast and US East Coast.

This World Cup-related demand comes on top of normal summer retail restocking, e-commerce promotions and earlier shipments ahead of possible tariff or cost increases.

As a result, the US routes are being supported by several demand drivers at the same time.

Red Sea diversions continue to absorb capacity

Beyond the US routes, the broader market is also being supported by continued Red Sea diversions.

Many Asia–Europe services are still avoiding the Red Sea and sailing around the Cape of Good Hope. Longer voyages reduce vessel turnaround efficiency and absorb more capacity.

This is important because the container shipping market has been worried about newbuilding deliveries and oversupply. However, the actual available capacity is being reduced by longer routes, schedule disruption, port-window pressure and slower empty container repositioning.

In other words, nominal capacity may be rising, but effective capacity remains tight in some key trades.

Fuel costs and geopolitical risks lift the cost base

Fuel prices and geopolitical risks are also supporting higher freight rates.

Tensions in the Middle East and concerns around the Strait of Hormuz have increased market uncertainty. For long-haul container routes, fuel is a major cost item. When bunker prices rise, carriers usually pass part of the cost to customers through bunker surcharges, peak season surcharges and FAK rate increases.

Several carriers have already announced new rate increases and surcharges on Asia–Europe, Asia–Mediterranean and transpacific services. Drewry reported that MSC planned to raise FAK rates from Asia to North Europe to USD 6,000 per 40ft container and from Asia to the West Mediterranean to USD 6,500 per 40ft container from June 15. CMA CGM and ONE also announced peak season surcharges of USD 500 to USD 600 per 20ft container from June 15.

Some actual booking costs exceed USD 10,000

The rise in index rates does not fully show what shippers are paying on some routes.

Market and freight forwarding sources indicate that, in early July, some Far East to Mediterranean, Black Sea and North Africa shipments have seen total booking costs exceed USD 10,000 per 40ft container after FAK rates, peak season surcharges, bunker charges, emissions-related charges and other surcharges are included.

This does not mean that all major routes have reached USD 10,000. SCFI and WCI reflect average rates on representative routes. Actual booking costs depend on the carrier, destination port, sailing date, space availability and surcharge structure.

For shippers, the real cost pressure can be higher than the index movement suggests.

Not driven by blank sailings alone

This rally is not mainly driven by large-scale blank sailings.

Drewry data shows that blank sailings on the transpacific route remain limited, with overall capacity relatively stable. The stronger driver is the combined effect of earlier cargo movement, Red Sea diversions, higher fuel costs, geopolitical risk and carrier surcharges.

The container shipping market is not back to the extreme conditions seen during the pandemic. But on some major routes and sailing windows, shippers are again facing tighter space and stronger carrier pricing.

Market enters a sensitive phase again

From 1,875.26 points in late April to 2,985.22 points on June 12, the SCFI has risen by nearly 60% in less than two months.

This shows that the container market remains highly sensitive.

Vessel supply is only one part of the equation. Route safety, geopolitical risk, fuel costs, port efficiency, empty container flows and cargo timing can all change effective capacity quickly.

For shippers, booking costs may remain high in the short term, especially on the US, Europe and Mediterranean routes. For carriers, the rally shows that the market has not returned to a low-volatility environment.

The next few weeks will be important. Freight rates will depend on whether early shipments continue, whether Red Sea and Middle East risks ease, and whether carriers can maintain pricing discipline.

For now, container freight rates are clearly back on an upward track.

READ MORE

Containers

Containers

Ningbo Containerized Freight Index Weekly Commentary Freight Rate Trends Diverged Across Routes; Composite Index Edged Up

Containers

Containers

European Route Freight Rates Enter a "Stepped Consolidation Phase"; Mid-July Rate Increase Window Remains Open

Containers

Containers