Phased Unblocking of Hormuz: Global Shipping and Oil & Gas Markets Enter a "Temporary Restart Window"

According to Xinde Marine News, in June 2026, the global energy and shipping markets reached a critical turning point centered around the Strait of Hormuz.

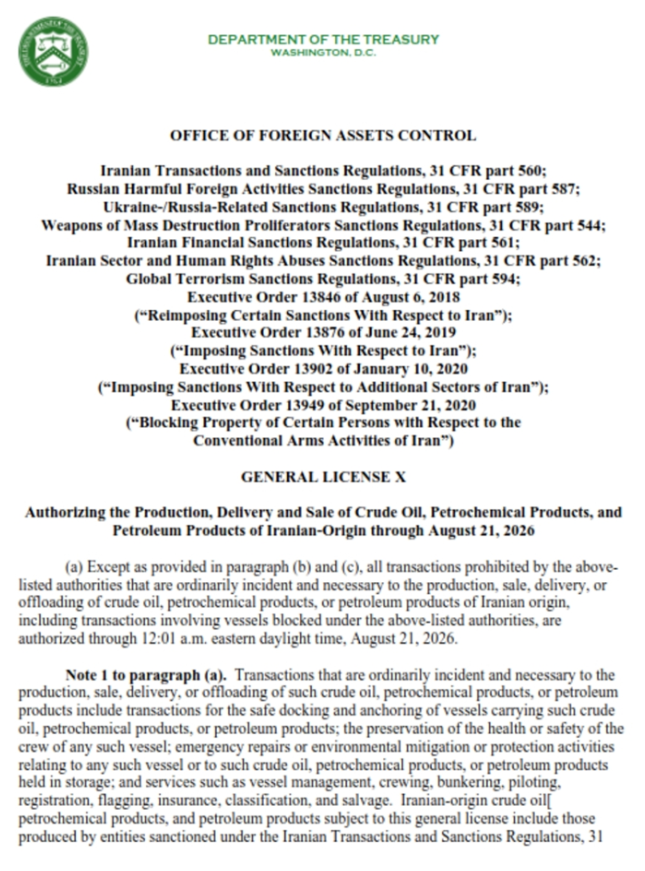

The U.S. Department of the Treasury's Office of Foreign Assets Control (OFAC) issued the Iran-related "General License X" (GL X) on June 22. This license authorizes certain transactions related to the production, sale, delivery, and offloading of crude oil, petrochemicals, and petroleum products of Iranian origin. The authorization is valid until 12:01 a.m. Eastern Daylight Time on August 21, 2026.

Meanwhile, the International Maritime Organization (IMO) announced the launch of a massive evacuation plan involving approximately 11,000 seafarers. This initiative aims to help commercial vessels and crews still stranded in the Gulf region to safely depart via the Strait of Hormuz.

The combination of these two arrangements signifies that the Strait of Hormuz is transitioning from a highly restricted state to a limited recovery. However, for the global shipping and oil and gas markets, this change does not equate to a "return to normal." More accurately, the market is entering a "temporary restart window" determined jointly by short-term sanctions waivers, safe evacuations, temporary shipping lanes, insurance assessments, and shipowners' risk appetites.

60-Day Compliance Window Opens, But the Market Remains Hesitant to Declare a Recovery

According to the GL X issued by OFAC, the authorization covers the production, sale, delivery, and offloading of Iranian-origin crude oil, petrochemicals, and petroleum products. It also includes certain services ordinarily incident and necessary to these transactions, such as safe berthing, anchoring, crew health and safety guarantees, emergency repairs, environmental protection, ship management, manning, bunkering, piloting, registration, flagging, insurance, classification, and salvage.

The license also specifies that payments owed to Iran, the Iranian government, or relevant blocked persons in these authorized transactions can be made using U.S. dollar-denominated funds. This point directly impacts trade settlements, banking compliance, shipping services, and insurance arrangements.

From the perspective of the shipping market, the significance of GL X is three-fold:

First, it opens a short-term compliance window for some Iranian oil trade. Oil flows, shipping services, and financial settlements previously suppressed by sanctions risks have been temporarily authorized within a specific scope.

Second, it reduces compliance uncertainty for certain auxiliary shipping services. Sectors such as ship management, crewing, bunkering, insurance, classification, and piloting previously faced extremely high risks when dealing with Iran-related cargoes, but now have clearer operational leeway within the authorized scope.

Third, it does not lift all sanctions. GL X states that this license does not authorize transactions involving North Korea, Cuba, specific restricted regions of Ukraine, Crimea, or other targets/regions, nor does it authorize activities still prohibited by U.S. laws and executive orders. Therefore, shipowners, charterers, traders, banks, and insurance institutions must still conduct strict due diligence.

This implies that GL X is not a comprehensive "lifting of the ban," but a policy window with a time limit, boundaries, and conditions. For shipowners and traders, the real question is not just "what can be done now," but also "what happens after August 21."

IMO Evacuation Action Indicates the Strait Remains Under Strict Control

Advancing in tandem with the OFAC policy window is the large-scale seafarer evacuation operation led by the IMO.

IMO Secretary-General Arsenio Dominguez stated that the evacuation plan will be carried out in cooperation with Iran, Oman, regional coastal states, the United States, and the shipping industry. The IMO stated that it has secured the necessary security guarantees and verified the safe navigational conditions supporting the evacuation operation.

This statement itself releases two important signals:

On one hand, the resumption of navigation has met certain political and security conditions. Otherwise, the IMO could not facilitate such a large-scale evacuation of personnel and vessels.

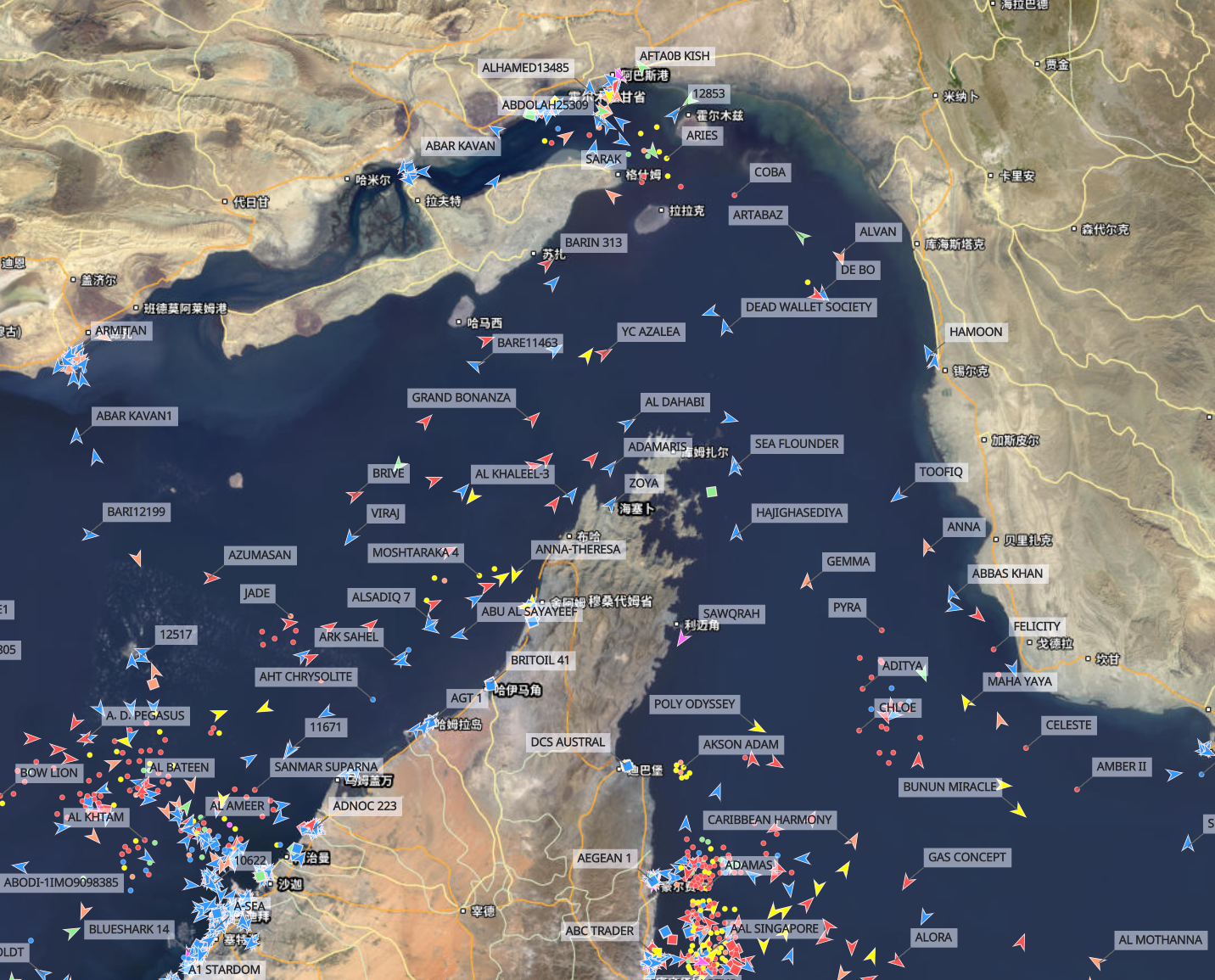

On the other hand, transit through the strait is still far from returning to routine conditions. According to Reuters, citing a notice from the Omani Ministry of Defense, the risk of collision remains high in the current environment, making the traditional Traffic Separation Scheme (TSS) temporarily unsafe. The evacuation operation will utilize temporary routes located to the north and south of the original TSS. Vessels will be contacted individually and assigned specific transit dates by the IMO coordinating body.

This demonstrates that the Strait of Hormuz is not experiencing a simple "reopening," but has entered a state of controlled transit. Vessels cannot freely enter and exit at the pre-crisis pace; instead, they must wait for batch scheduling, route confirmation, and security assessments.

For shipping companies, while this model helps mitigate short-term security risks, it also means that transit efficiency cannot recover quickly. Large commercial vessels waiting, queuing, diverting, slowing down, and being dispatched at both ends of the strait will continue to drive up actual transportation costs.

Tankers and LNG Carriers Pioneer the Recovery as the Energy Shipping Market Reacts Quickly

In terms of vessel types, tankers and LNG carriers are the first sectors to show clear signs of recovery.

Reuters, citing vessel tracking data, reported that several previously stranded VLCCs have left via the Strait of Hormuz, and some Qatar-related unladen LNG carriers have begun re-entering the Gulf to prepare for loading. Relevant data also shows that QatarEnergy-related LNG carriers gradually entered the strait from mid-to-late June, representing a rare influx of returning LNG vessels since the conflict began.

This change reflects the commercial logic of the energy shipping market. Tankers and LNG carriers transport high-value cargoes with rigid demand. Once policy and security conditions show marginal improvement, traders, refineries, and energy companies quickly assess the feasibility of resuming loading. For shipowners, as long as freight rates, war risk insurance, and cargo owner commitments are sufficient to cover the risks, some vessels will be the first to attempt entry and exit.

However, the recovery is uneven. According to a Reuters report, transit volumes through Hormuz remain far below the pre-conflict average of about 125 vessels per day. Concurrently, mine risks, restricted main channels, insurance costs, and vessel availability continue to constrain market recovery.

The reaction in tanker freight rates is particularly noticeable. Reuters reported that as Middle Eastern oil-producing countries increase exports and vessel demand rises, charter rates for tankers entering Hormuz and related Gulf routes surged significantly within a week. The estimated daily earnings for some VLCC voyages loading in the Gulf and departing via Hormuz have reached extremely high levels. War risk insurance costs have retreated from their peak but remain significantly higher than normal periods.

This indicates that the partial restart of the strait has not immediately lowered tanker transportation costs. On the contrary, with many vessels still stranded, tight available capacity, and cargo owners eager to resume loading, the tanker market may experience an anomalous combination of "resumed transit and rising freight rates" in the short term.

Container Shipping Recovers the Slowest; Liner Networks Enter a Three-Stage Restructuring

Compared to tankers and LNG carriers, the recovery pace for container shipping lines will be noticeably slower.

The reason is that container shipping is not a single-ship, single-cargo, single-voyage transaction, but a global network system. Whether an ocean-going mainline service can enter the Gulf affects sailing schedules, slot availability, empty containers, port windows, feeder connections, customer deliveries, and global capacity turnaround.

Xeneta data shows that before the crisis, 99 container services operated in or passed through the Arabian Gulf, deploying a total nominal capacity of about 3.2 million TEUs, which accounted for approximately 10% of the global container fleet capacity. Following the blockade, only 11 services remained operational within the region, totaling about 74,000 TEUs. Out of 488 vessels deployed on relevant services prior to the crisis, only 18 remain on Arabian Gulf routes, while the other 470 have been diverted or reallocated across the global network.

Network disruption on this scale cannot be instantly resolved by a phased agreement.

Xeneta suggests that the recovery of the container network will go through three stages:

"Stage 0" focuses on saving vessels and personnel. Vessels that have been stranded in the Arabian Gulf for a long time must be evacuated first. Issues regarding reefer cargoes, dangerous goods, equipment status, crew changes, and port congestion all need to be addressed individually.

Recovery of regional feeder services. Smaller feeder vessels will be the first to rebuild connections between ports within the Arabian Gulf. Compared to ocean-going mother ships, feeder vessels have a smaller risk exposure; even if the situation deteriorates again, the collateral impact on the global mainline network is more manageable.

Return of ocean-going mainlines. For major long-haul services like Asia-Europe and Asia-North America to deeply re-enter the Gulf, confirmation is required regarding the security situation, insurance premium rates, demining progress, port order, and customer demand.

Therefore, the real focus for the container market is not "whether Hormuz is navigable," but "whether carriers are willing to push their mainlines deep into the Gulf again."

Even if the strait gradually recovers, liner companies are highly likely to adjust their Middle East service structures. In the future, more cargo may be transshipped through ports outside the Gulf or via nodes like the Red Sea and Oman, before entering the inner Gulf market via regional feeders. While this increases transit time and transshipment costs, it reduces the probability of mainlines being dragged into high-risk waters by sudden blockades.

This will become a major change in the Middle Eastern container network. In the past, the market pursued direct calls, scale, and efficiency; after experiencing the Hormuz crisis, carriers and cargo owners will place greater emphasis on redundancy, alternative routes, and network resilience.

Freight Rates Will Not Fall Quickly; Risk Premiums Will Remain in the Market

Following the phased restart of Hormuz, some market participants expected oil prices and freight rates to drop rapidly. However, judging from the current situation, a decline in shipping costs may not occur synchronously.

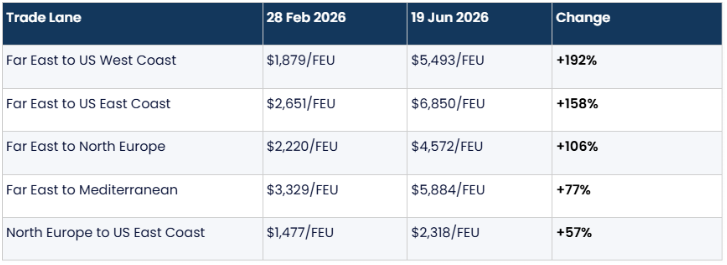

The container market has already exhibited obvious spillover effects. Xeneta data reveals that even mainline routes not directly passing through Hormuz have been affected by the withdrawal of Middle Eastern capacity and global slot mismatches. Spot freight rates for the Far East to U.S. West Coast route rose from $1,879/FEU at the end of February to $5,493/FEU on June 19, an increase of 192%. The Far East to Northern Europe route increased from $2,220/FEU to $4,572/FEU, a 106% jump.

This shows that the Hormuz crisis affects more than just local Middle Eastern routes. When roughly 10% of global container capacity is implicated, carriers must withdraw vessels, change ports, reroute, and reschedule networks from other routes, transmitting freight rate pressure to the Pacific, Asia-Europe, Mediterranean, and Atlantic trades.

The tanker market faces similar issues. Although expectations of restored energy supplies may depress oil prices, tanker freight rates, war risk insurance, waiting times, and vessel availability will drive up actual delivery costs in the short term. Especially with vessels still stranded inside the Gulf, the main channel not fully restored, and oil-producing countries collectively releasing export demand, tanker capacity supply and demand may remain tight.

Therefore, in the coming weeks or even months, the market may experience a complex state:

Crude oil prices are falling, but shipping costs remain high.

The waterway is nominally open, but schedule reliability has not recovered.

Ports are resuming loading, but insurance and compliance reviews are still significantly slowing down the pace of transactions.

The Oil and Gas Distribution Market Enters a Repricing Phase

The Strait of Hormuz is one of the world's most critical oil and gas chokepoints. For Asian refineries, LNG buyers, and Middle Eastern energy exporters, the phased restart will provide a significant buffer.

For Asian buyers such as India, China, Japan, and South Korea, GL X provides room to reassess Iranian petroleum products and Middle Eastern supplies. Some trade demand previously backlogged by sanctions, war, and navigational risks is expected to be released within the 60-day window.

However, buyers will not simply revert to the pre-crisis mode. Following prolonged blockades and transit uncertainties, refineries and traders will place higher importance on contract flexibility, alternative sources, inventory security, and the diversification of transportation routes.

In the LNG market, the re-entry of Qatar-related LNG carriers into the Gulf is a positive signal. Qatar is one of the world's most important LNG exporters, and the resumption of loading at core nodes like Ras Laffan is highly significant for the stability of gas supplies to Asia and Europe. Nevertheless, due to the high asset value of LNG carriers, complex voyage planning, and strict terminal receiving windows, the recovery of LNG transportation will still proceed at a relatively cautious pace.

For refined oil, chemicals, and petrochemicals, the recovery speed may be slower than that of crude oil. Relevant supply chains involve contract supplies, inventory digestion, downstream demand, vessel matching, and port operations. Furthermore, both buyers and sellers will be concerned about policy changes once the 60-day window closes. In the short term, even if certain markets have the conditions to recover, they may remain on the sidelines due to the risk of reinstated sanctions.

The True Impact on Global Supply Chains: Long-Term Risk Premiums

The phased unblocking of the Strait of Hormuz has bought a breathing window for the global shipping and energy markets. Trapped vessels can gradually evacuate, some oil and gas flows can resume, and liner companies can begin redesigning their Middle East service networks.

However, the nature of this window remains temporary, fragile, and reversible.

The 60-day license, temporary safe channels, vessel-by-vessel transit date allocations, unresolved waterway risks, high insurance rates, and the assessment that liner network recovery will take months all point to the same conclusion: the market is far from returning to its pre-crisis state.

For shipping companies, energy traders, and cargo owners, the most critical observation points in the near future include four aspects:

First, whether GL X will be extended after expiration or replaced by a new long-term agreement.

Second, whether the Strait of Hormuz can transition from temporary security guarantees to a stable transit mechanism.

Third, whether war risk insurance, tanker freight rates, and container spot rates can meaningfully decline.

Fourth, whether liner companies will permanently increase the proportion of transshipments outside the Gulf and regional feeder services.

Following the Red Sea crisis, Panama Canal transit restrictions, the Black Sea conflict, and the Hormuz blockade, the global shipping industry's assumption of the "stable opening of key chokepoints" is being re-evaluated. For shipowners, capacity redundancy and route optionality are becoming part of asset value. For cargo owners, the lowest freight rate is no longer the sole metric; the importance of delivery certainty, alternative routes, and inventory arrangements has risen significantly. For energy buyers, procurement costs include not just oil or gas prices, but also insurance, freight, transit risks, and policy uncertainties.

The phased unblocking of the Strait of Hormuz is certainly a positive signal. But what it truly reveals is that global shipping and oil and gas markets are entering a new risk-pricing cycle.

Future market competition will no longer be just about who can run the fastest during stable periods. It will also be about who can keep their supply chains intact when straits close, war risk premiums soar, ports shut down, and policy windows rapidly shift.

READ MORE

Safety

Safety

Deadly Mooring Ropes: The "Super Cycle" of South Korea's Shipbuilding Industry

Safety

Safety

Vessel Traffic Returns! Transit Volumes in the Strait of Hormuz Rebound Significantly

Safety

Safety

OFAC General License X brings tankers, insurance, class and maritime services into temporary authorization

Safety

Safety

8,500 TEU EVER LOVELY Hit Off Oman as IMO Pauses Hormuz Seafarer Evacuation Operation

Safety

Safety

Is Transiting the Strait of Hormuz Really Free? A Bigger Bill May Be Waiting

Safety

Safety