During Singapore Maritime Week, Mitsui O.S.K. Lines, Ltd. (MOL) held a media briefing at its Singapore office on 22 April, where newly appointed President and CEO Jotaro Tamura made one of his first major media appearances in the region.

For MOL, this was more than a routine corporate update. It was a clear statement of direction from its new leader: MOL will continue to build on its traditional shipping foundation, while accelerating its transformation into what it calls a “global social infrastructure company.”

Singapore chosen as the first stop

Tamura said that after taking over as president and CEO, he had started a global tour to meet stakeholders in different regions. His first stop was Singapore.

The choice was deliberate. According to Tamura, Singapore is MOL’s second-largest organization within its global network. Around one year ago, MOL designated Singapore as its “sub-headquarters,” reflecting the city-state’s growing importance not only as a maritime hub, but also as a base for MOL’s business development across Southeast Asia, Oceania and the wider Indian Ocean region.

This also aligns closely with MOL’s newly updated corporate management plan, “BLUE ACTION 2035 Phase 2,” which covers fiscal years 2026 to 2030. While Phase 1, from 2023 to 2025, focused on “transformation and expansion,” Phase 2 is positioned as a period of “value realization.”

In other words, MOL is now moving from large-scale investment and portfolio reshaping toward profit delivery, capital discipline, stronger shareholder returns and deeper regional execution.

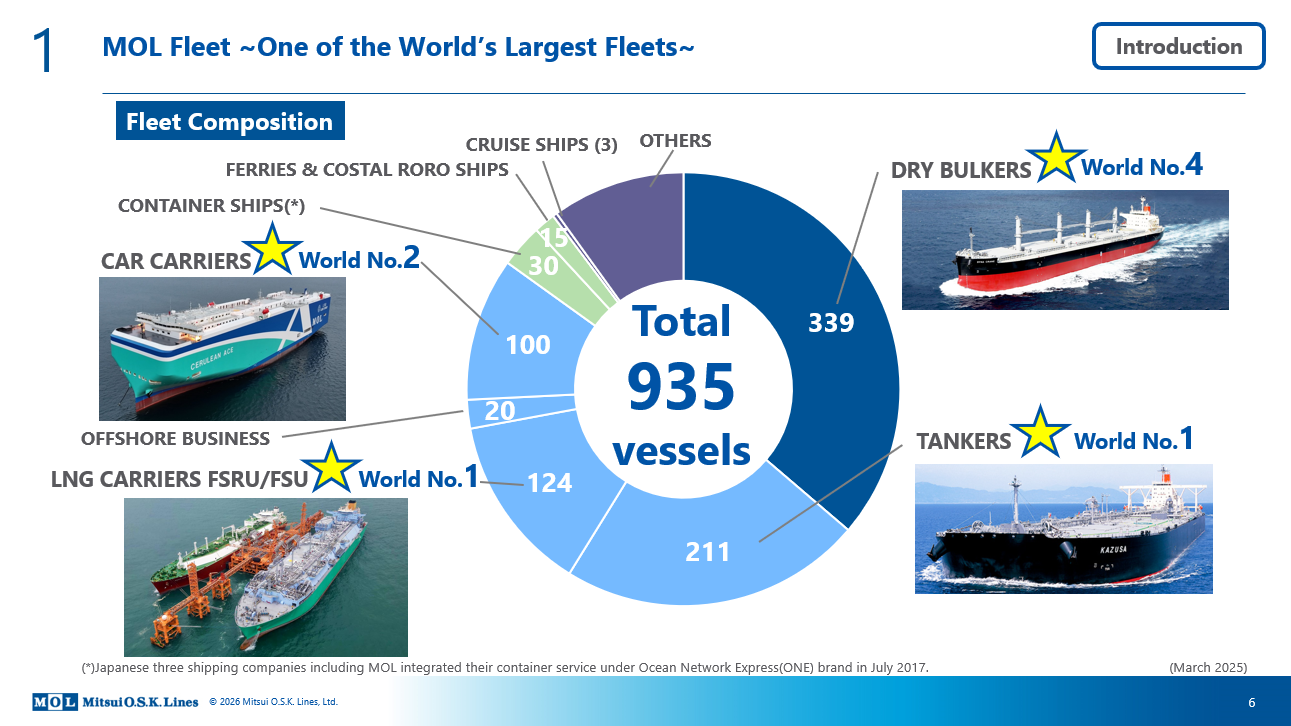

A 935-vessel global platform

Tamura began by setting out the scale of MOL’s fleet and business platform.

As of 2025, MOL operates 935 vessels across multiple shipping segments. These include 339 dry bulk carriers, ranking the company fourth globally in dry bulk; 211 tankers, ranking first globally; 124 LNG-related vessels, making MOL one of the world’s leading LNG carrier operators; and 100 car carriers, ranking second globally.

The company’s container ship number appears much smaller, at 30 vessels, but Tamura explained that this is because the container liner business of Japan’s three major shipping companies was spun out into Ocean Network Express (ONE) in 2017. MOL still owns and charters container vessels to ONE, while ONE itself acts as the container operator.

This structure also shapes MOL’s broader logistics strategy. In response to a media question, Tamura explained that ONE focuses on container shipping and container terminals, while forwarding, warehousing, trucking and related logistics activities remain largely within MOL, NYK and K Line.

This means MOL’s container exposure has not disappeared. Rather, it has been reorganized through ONE, while MOL itself continues to build a broader portfolio around shipping, energy transportation, logistics, terminals and infrastructure.

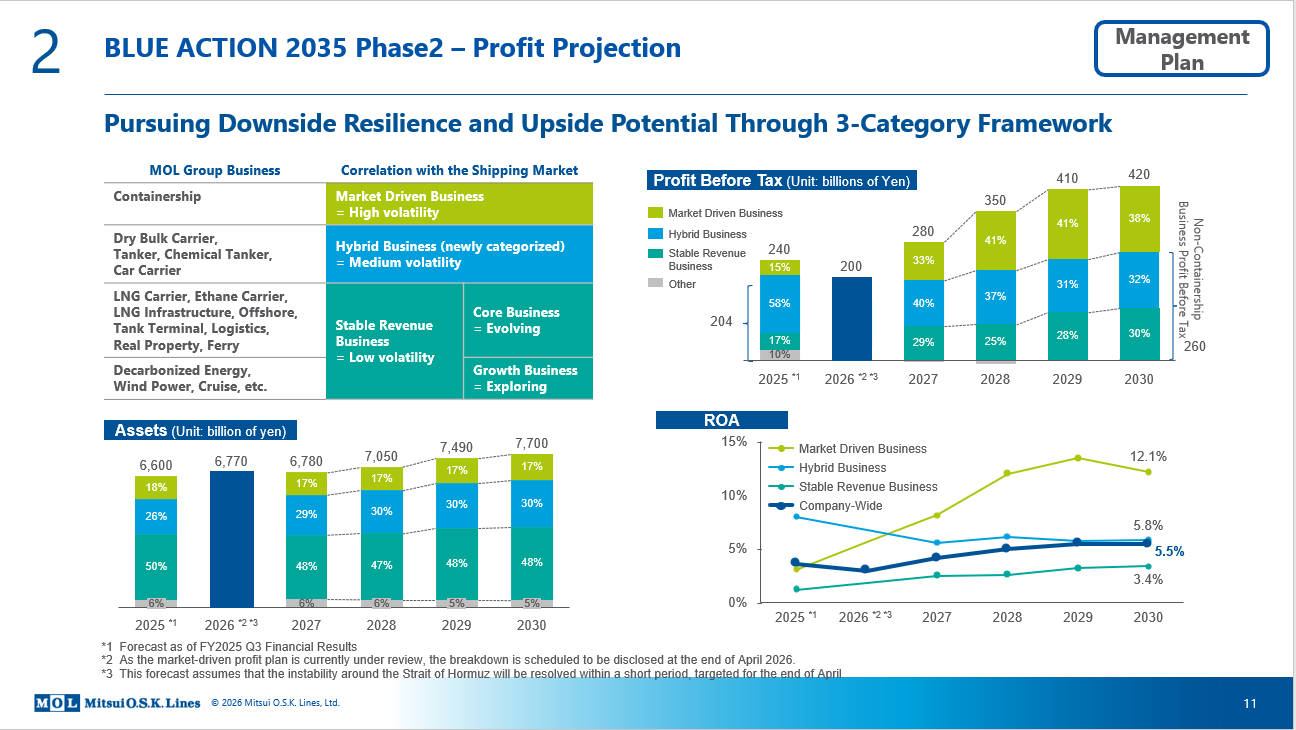

Targeting ¥420 billion in profit before tax by 2030

Under “BLUE ACTION 2035 Phase 2,” MOL expects its profit before tax to rise from a forecast ¥240 billion in FY2025 to ¥420 billion by FY2030. By FY2035, the company has lifted its longer-term target to ¥500 billion.

The key to this plan is portfolio transformation.

During Phase 1, MOL executed around ¥2 trillion in investments, significantly above its original plan of ¥1.2 trillion. Of that amount, about ¥1.6 trillion was allocated to stable revenue businesses.

As a result, the company’s asset mix has shifted materially. The ratio of market-driven businesses to stable revenue businesses moved from 51:49 in FY2022 to an expected 37:63 in FY2025.

This is important for a shipping group that has historically been exposed to volatile freight markets. MOL is not abandoning market-driven businesses, but it is building a stronger base of long-term, lower-volatility earnings through LNG carriers, ethane carriers, LNG infrastructure, offshore, tank terminals, logistics, real estate, ferries and other infrastructure-style businesses.

Three business categories: market-driven, hybrid and stable revenue

MOL has introduced a three-category business framework for Phase 2.

The first category is market-driven business, mainly container shipping. This business has high exposure to freight market cycles, but can generate strong upside during market surges.

The second category is “hybrid business,” newly defined by MOL. This includes dry bulk carriers, tankers, chemical tankers and car carriers. These businesses still have market exposure, but also benefit from long-term customer relationships, specialized vessel types, route-specific advantages and contract coverage.

The third category is stable revenue business, including LNG carriers, ethane carriers, LNG infrastructure, offshore, tank terminals, logistics, real property and ferries. These are businesses with long-term contracts or limited earnings volatility.

MOL is also treating decarbonized energy, wind power and cruise as growth businesses for future development.

The overall direction is clear: MOL wants to retain market upside, but reduce downside risk. It is building a portfolio that can perform through cycles, rather than relying only on freight market timing.

Capital allocation: investment, asset recycling and stronger shareholder returns

For FY2026 to FY2030, MOL expects total cash inflow and cash outflow of ¥2.88 trillion.

Business investment will remain the largest use of funds, totaling about ¥2.34 trillion. This includes ¥830 billion in projects already decided during Phase 1, plus ¥1.51 trillion in new Phase 2 investment plans.

The already-decided projects include ¥230 billion in dry bulk, involving 18 environmentally friendly, state-of-the-art vessels; ¥320 billion in energy, involving 53 newbuildings including LNG and LPG carriers; ¥90 billion in chemical logistics, mainly tank terminal investments; ¥40 billion in product transportation, including three environmentally friendly car carriers; and ¥140 billion in wellbeing lifestyle, mainly domestic real estate redevelopment projects.

At the same time, MOL is strengthening shareholder returns. From FY2026, the company plans to introduce progressive dividends starting at ¥205 per share, together with flexible share buybacks, targeting a total payout ratio of around 40%.

This marks a shift from rapid expansion toward disciplined value delivery.

Singapore as a regional growth platform

Tamura also highlighted three examples of MOL’s business expansion in Singapore.

The first is logistics and high-value warehousing. MOL is involved in the 8 Jalan Besut warehouse and is also participating with CapitaLand Group in the development of the highly automated logistics facility “OMEGA 1 Singapore.” These are not traditional shipping assets, but they support MOL’s goal of converting stable logistics demand in Southeast Asia into long-term earnings.

The second is energy infrastructure. MOL has secured a long-term FSRU-related project to support Singapore’s energy security, with service expected to begin in 2029. This fits directly into MOL’s strategy of developing stable, long-term energy infrastructure businesses.

The third is car carrier terminal operations. MOL has announced cooperation with PSA to establish a car carrier terminal operating company in Singapore. This will connect MOL’s car carrier strength with terminal infrastructure, creating a more integrated automotive logistics platform.

These examples show that MOL’s Singapore office is not merely a regional branch. It is becoming a platform for business development across shipping, energy, logistics and infrastructure.

Xinde Marine asks about China: “The relationship has been good, is good, and we hope it continues”

During the Q&A session, Xinde Marine asked Tamura about China.

The question focused on MOL’s existing and future cooperation with China, including Chinese energy companies, shipping companies and the shipbuilding industry. Although the briefing was held in Singapore, China remains one of the most important markets in global shipping, energy transportation, shipbuilding and maritime supply chains.

Tamura responded clearly. He said the business relationship between MOL and Chinese stakeholders “has been good, is good, and we hope that continues.”

He mentioned Chinese customers such as CNOOC, as well as shipping partners such as COSCO, noting that MOL maintains close relationships with a number of Chinese stakeholders.

Tamura acknowledged that geopolitical developments affect all global businesses. However, as a global ship operator, MOL wants to continue doing business with China, including services and projects.

He also disclosed that he had been in China just the previous week for a newbuilding-related event and had held discussions with local stakeholders.

This answer is significant. For a company like MOL, China is not only a cargo and energy demand market. It is also one of the world’s most important shipbuilding centers and a critical part of the global maritime industrial chain.

As MOL continues to invest in LNG carriers, tankers, dry bulk carriers, car carriers and low-carbon vessels, cooperation with Chinese shipyards, energy companies and shipping groups will likely remain an important part of its long-term strategy.

Net zero: a long and winding road

On decarbonization, Tamura emphasized that MOL’s long-term commitment remains unchanged. The company declared its 2050 net-zero target in 2021 and continues to work toward that goal.

However, he also described the pathway as “a long and winding road.” Geopolitics, fuel prices, technology, fuel supply chains and regulation will all make the transition more complex.

For the short term, Tamura said MOL will continue doing what it can and what it should do. That includes fuel-saving measures, operational efficiency improvements and practical energy-saving technologies, while waiting for further development in alternative fuel supply chains and technology.

On future fuels, MOL is keeping an open position. Tamura said the company is looking at LNG, ammonia, ethanol, biofuels and other options, because it is still too early to determine which fuel will become the future standard.

This is a pragmatic position. The industry is moving toward decarbonization, but fuel availability, lifecycle emissions accounting, cost, bunkering infrastructure and engine technology remain uncertain. For major shipowners, flexibility is becoming a form of risk management.

LNG remains a practical transition solution

Tamura also addressed LNG and the wider energy transportation outlook.

He said LNG has been proven as a practical solution for shipping, especially when compared with fuels that are still at an earlier stage of commercial development. LNG already has a more mature supply chain, established vessel technology and real-world operating experience.

At the same time, he noted that the current geopolitical situation, particularly around energy security and the Middle East, could affect the future of energy transportation. Countries may need to review sourcing strategies, stockpiling policies and supply chain resilience.

From a shipping perspective, this could create more demand for longer-distance sourcing, higher inventories and more diversified trade flows. However, if energy and bunker prices remain high, that could also slow the adoption of new fuels.

This reflects one of MOL’s core assumptions in its latest management plan: geopolitical risk, energy security and the reevaluation of LNG as a practical solution are now central factors shaping the shipping industry.

From shipping company to social infrastructure company

The message from MOL’s Singapore briefing was consistent.

MOL remains deeply rooted in shipping. Its 935-vessel fleet is still the foundation of the group’s global influence. Dry bulk, tankers, LNG and car carriers remain major pillars.

But MOL no longer sees itself only as a traditional shipping company. It is expanding around vessels, ports, energy, logistics, warehouses, terminals, offshore assets, low-carbon fuels and regional infrastructure.

For the wider shipping industry, MOL’s strategy is representative of a broader shift. In an era of geopolitical uncertainty, energy transition, supply chain fragmentation and rising resilience requirements, the competitive advantage of major shipping groups is no longer measured only by vessel numbers or freight market exposure.

It is increasingly measured by portfolio quality, regional networks, long-term contracts, infrastructure positions, customer relationships and the ability to organize supply chains.

For MOL’s new chief, the next five years will be about turning previous investment into visible results. The company wants to continue operating through shipping cycles, but with less dependence on them. It wants to invest in vessels, but also in infrastructure. It wants to serve global trade, but also position itself as part of the social infrastructure that keeps economies running.

The opinions expressed herein are the author's and not necessarily those of The Xinde Marine News.

Please Contact Us at:

media@xindemarine.com