Hong Kong based minor bulk specialist Pacific Basin revealed statistics during its latest quarterly trade update which have grown unfamiliar during the last three years of ever- improving figures.

Core business average handysize and supramax daily time-charter earnings of US$13,550 and US$13,630 net per day in the first quarter of 2022 represented a decrease of 43% and 58% compared to the first quarter of 2022.

Scrubber technology on 33 supramax vessels softened the blow, contributing US$1,320. per day to an outperformance of the market.

In what Pacific Basin management sense to be an imminent market improvement, for the second quarter of 2023 the company has covered 74% and 100% of our core committed vessel days at US$12,710 and US$14,080 net per day for Handysize and Supramax respectively. For the second half of 2023 Pacific Basin currently has cover for 25% and 45% of core vessel days at US$10,820 and US$13,490 net per day for Handysize and Supramax respectively.

Offering scenarios on the coming quarter and beyond the company said:

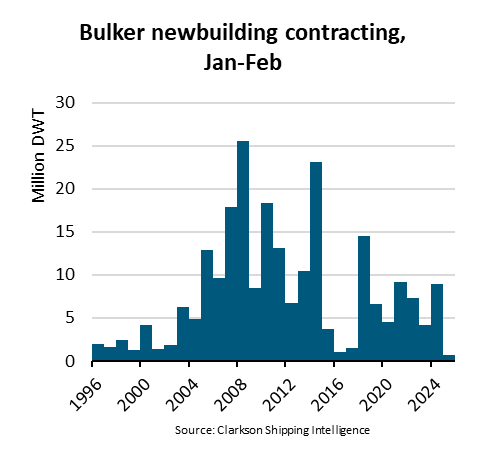

“Dry bulk ship ordering remained muted over the period despite increased newbuild ordering in other sectors. Shipyard slots remain limited, resulting in a new order placed today generally expected to be delivered in 2026.

According to Clarksons Research the overall dry bulk orderbook remains at a decades low 6.9% and ordering in the first quarter is down approximately 50% compared to the same period last year. We believe that the high cost of newbuildings, along with higher capital costs, will continue to deter newbuild ordering, when lower priced second-hand ships with prompt delivery represent a more attractive investment with lower residual value risk. We expect that ordering for dry bulk vessels will remain restrained going forward, discouraged by uncertainty about the future fuels, vessel designs and technology that will be required to meet decarbonisation regulations. We expect the ordering of dual-fuel zero-emission mid-size dry bulk vessels to be commercially feasible in late 2024 at the earliest.”

Pacific Basin expects IMO’s global EEXI (Energy Efficiency Existing Ship Index) and CII (Carbon Intensity Indicator) regulations came into effect in January 2023, will help slow capacity expansion. The regulations are expected to drive technical and operational measures to improve the carbon efficiency of existing ships. EEXI (and specifically engine power limiters) will result in a one-time permanent reduction in maximum speeds, which will limit the global fleet’s ability to speed up to meet increases in demand. CII will result in progressively slower vessel speeds and, over time, accelerated scrapping as older and less-efficient ships become incapable of compliance.

Ship recycling will also have a role in upholding the freight market, according to Pacific Basin.

“We expect scrapping to increase in coming years as environmental regulations will encourage owners to phase out older, less efficient ships. Handysize and Supramax vessels over 20 years old constitute approximately 14% and 10% of the global Handysize and Supramax fleet respectively, and are likely to be potential scrapping candidates. Clarksons Research currently forecasts scrapping of 1.4% and 2.1% for minor bulk ships in 2023 and 2024, with these supply-side developments to continue to support the freight market.”

Source:

Hong Kong Maritime Hub

The opinions expressed herein are the author's and not necessarily those of The Xinde Marine News.

Please Contact Us at:

media@xindemarine.com

.gif)

Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  BIMCO Shipping Number of the Week: Bulker newbuildi

BIMCO Shipping Number of the Week: Bulker newbuildi  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar  Ningbo Containerized Freight Index Weekly Commentar

Ningbo Containerized Freight Index Weekly Commentar