This is the second part of a two-part series looking at how COVID-19 has triggered contrasting fortunes in the global iron ore market. Part 1: Price bands narrow in year of contrasts

The coronavirus pandemic has triggered a sharp contraction in the global iron ore pellet trade in tandem with the slump in steel demand that has prompted aggressive cuts to steel and pig iron production outside of China in recent months.

The EU and Japan, both major iron ore importers, saw steel output fall 18%-19% year on year over January-September amid a wave of blast furnace capacity curtailments as downstream demand dried up.

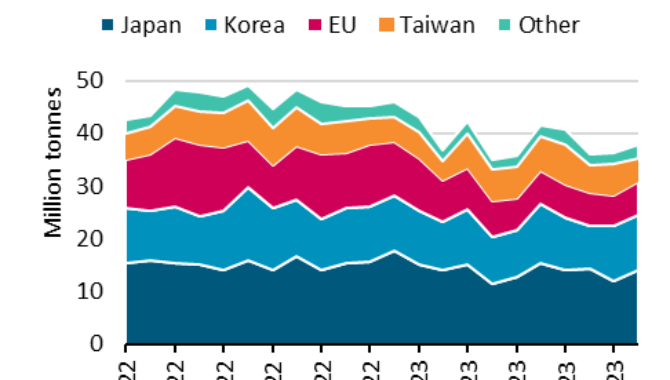

That decline in steel output has led to a pronounced fall in pellet trade. Over January-August, pellet imports by Japan and South Korea fell 38% and 42%, respectively, year on year, for a combined fall of 4.2 million mt, while the EU’s pellet imports fell 29%, or by 7 million mt, over the same period.

A reduced emphasis on boosting blast furnace productivity during the downturn has curtailed ex-China pellet demand. Pellets are also typically more expensive relative to iron ore fines and lump. Therefore, steel producers tend to scale back pellet usage as a cost reduction measure in a market downturn. Blast furnace-based steelmaking dominates in East Asia and Europe, where producers have scope to adjust and optimize the iron ore burden between sintered fines, lump and pellet products.

In the Middle East, direct reduced iron-based steelmaking is more prevalent, with DR-grade pellets accounting for most of the iron ore consumed. With steel production in Qatar and UAE scaled back aggressively, pellet trade has fallen sharply, with the UAE posting a 24% year-on-year fall in imports over January-August. Saudi Arabia saw pellet imports fall 13% year on year over the same period, mirroring the decline in domestic direct reduction iron production.

China is one of the few bright spots for the pellet trade in 2020, with January-August imports surging 93% year on year, equating to a 16 million mt increase. Economic recovery in China has led to a sharp rebound in steel demand.

This spurred Chinese steel production growth of 4.5% on year over January-September, National Bureau of Statistics data showed.

China’s blast furnace productivity drive, coupled with the prospect of seasonal restraints on sintering operations to curb winter emissions, would favor increased pellet usage in Chinese blast furnaces in the coming months.

The contrast of a resurgent Chinese steel market and ailing demand globally is reflected in a shift in trade patterns for pellet exporters. The downturn ex-China has prompted iron ore exporters to divert more supply to China, boosting pellet trade from Russia, Ukraine, Sweden and India.

Brazil is the world’s biggest exporter of pellets, despite a drop in shipments from 54 million mt in 2015 to 27 million mt in 2019. Key to this was the Fundão tailings dam disaster in late 2015, which led Samarco, a major pellet producer, to cease operating. Another pellet supply crunch ensued in 2019 after the collapse of Vale’s Brumadinho tailings dam, which tragically resulted in multiple fatalities. The first nine months of 2020 saw Brazilian pellet exports drop by 36%, or 6.6 million mt, year on year.

However, the trade looks set for a boost with Samarco planning to restart production in the current quarter, initially operating at 26% of its total 30.5 million mt/year capacity.

Pellet trade in North America is also in contraction mode, as aggressive steel production cuts have curtailed iron ore demand in the region. While US pellet exports fell 10% year on year in the first eight months of 2020, strong demand from China has driven Canadian pellet exports 3.3% higher. In the Middle East, pellet shipments from Bahrain fell 45% year on year, or 2.8 million mt, in the first eight months, while correspondingly robust steel production growth in Iran reduced its pellet exports by 2 million mt over the same period.

The slowdown in global pellet trade has unsurprisingly narrowed pellet price premiums. The Atlantic Basin blast furnace 65% Fe pellet premium has fallen to $27.50/dmt to date in October from $31/dmt in April and $37/dmt in the fourth quarter of 2019. Year to date, the Atlantic Basin premium has averaged just $29/dmt, compared with $57/dmt in 2019. Weak demand in the Middle East has seen the Platts DR-grade 67.5% Fe pellet premium slide to $30/dmt to date in October from $43.75/dmt in June and an average of $62/dmt over 2019.

Looking to 2021, S&P Global Market Intelligence expects a recovery in global economic growth to trigger a significant improvement in ex-China pellet demand. This will be led by a ramp-up in blast furnace output in Europe, Japan and India and a recovery in DRI production in the Middle East.

Pellet premiums are expected to rebound from current lows — although the upside could be tempered by rising pellet supply, boosted by the planned restart of Samarco’s pellet operations in Brazil.

Source:Platts

The opinions expressed herein are the author's and not necessarily those of The Xinde Marine News.

Please Contact Us at:

media@xindemarine.com

.gif)

PIL launches Academy to strengthen workforce compet

PIL launches Academy to strengthen workforce compet  Coal shipments to advanced economies down 17% so fa

Coal shipments to advanced economies down 17% so fa  China futures market updates at close (Nov 14)

China futures market updates at close (Nov 14)  CISA: China's daily crude steel output down 5.7% in

CISA: China's daily crude steel output down 5.7% in  China futures market updates at close (Oct 31)

China futures market updates at close (Oct 31)  CISA: China's daily crude steel output down 1.2% in

CISA: China's daily crude steel output down 1.2% in