China is set to record another month of strong iron ore imports in August, helping to justify the ongoing resilience in the price of the main ingredient in steel.

What’s harder to quantify is exactly what’s happening to all the steel being produced.

China’s seaborne imports of iron ore were 92.9 million tonnes, with one day left to assess cargo arrivals, according to Refinitiv vessel-tracking and port data.

Even if this figure does increase somewhat, it’s unlikely to reach the record 112.65 million tonnes reported by customs for July, however, it will be in line with the average monthly imports of 94.23 million tonnes for the first seven months of the year.

The strength in China’s iron ore imports, which rose 11.8% in the first seven months of 2020 compared to the same period a year earlier, has been one of the bright spots in the economic recovery from the lockdowns imposed to curb the spread of the novel coronavirus.

Steel output has also been robust, hitting a monthly record of 93.36 million tonnes in July, according to official figures. On a per day basis, July’s output of 3.01 million tonnes was just below the record 3.05 million achieved in June.

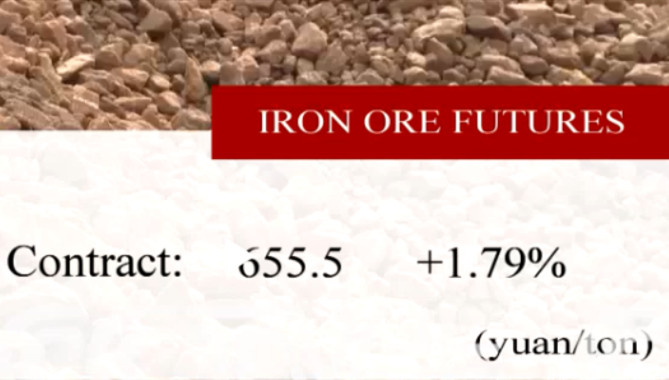

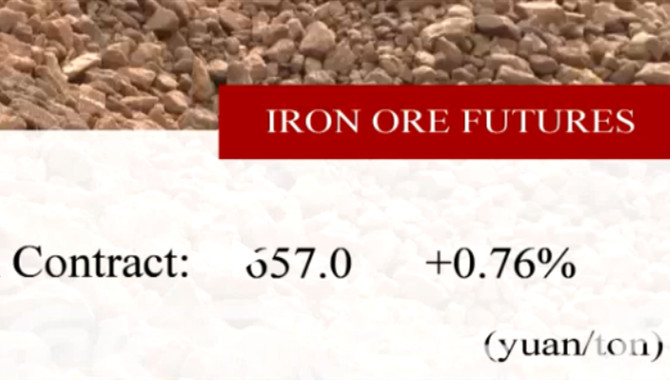

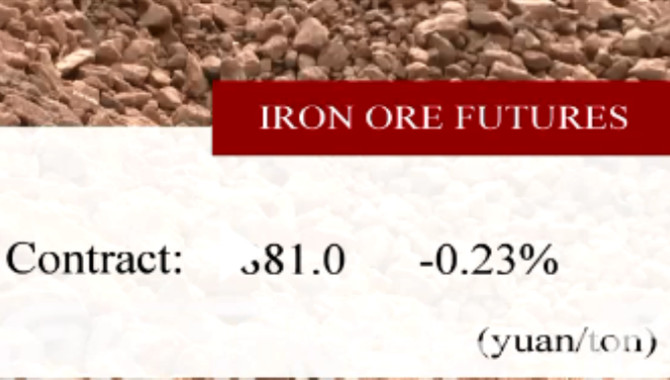

The strong demand for iron ore has seen the spot price for benchmark 62% iron ore delivered to north China MT-IO-QIN62=ARG, as assessed by commodity price reporting agency Argus, surge 62% from its low so far this year of $79.60 a tonne on March 23 to its recent 6 1/2-year high of $128.60.

The price has since slipped slightly to end at $123.45 a tonne on Aug. 28, but remains high by the standards of the previous five years.

The price of benchmark steel rebar futures in Shanghai have also been robust, but not in the league of iron ore’s gains.

The contract ended at 3,717 yuan ($541.84) a tonne on Aug. 28, up 22% from the closing low so far this year of 3,059 yuan on Feb. 3.

The outperformance of iron ore over steel has led to a contraction of margins in the industry, as seen by the 37% slump in profits in the first six months of 2020 announced by top steel marker Baoshan Iron and Steel.

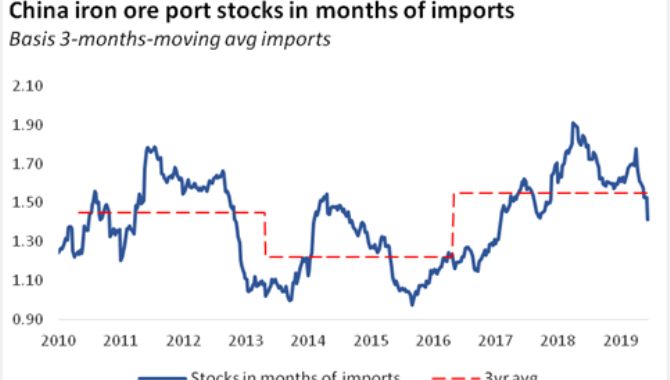

But this has yet to result in steel mills curbing output, even though there are signs that inventories are starting to rise.

Stocks of rebar SH-TOT-RBARINV, as measured by consultants SteelHome, rose to 7.94 million tonnes in the week ended Aug. 28, up from the low for the year so far of 7.1 million tonnes for the week to June 24.

However, given the cyclical nature of China’s steel inventories, which tend to rise sharply at the end of the year and then draw down as construction ramps up as winter ends, it’s more important to compare inventory levels to where they were at the same point in prior years.

At the end of August 2019, inventories were 5.81 million tonnes, at end August 2018 they were 4.15 million and at the same time in 2017 they were 3.88 million.

This suggests that rebar inventories are elevated for the time of year, and that’s just the visible inventories that can be monitored.

DARK WAREHOUSES

One of the unknowns in China is how much steel is sitting in stockpiles that aren’t being assessed, the so-called dark warehouses where traders can store metal that they are financing in the expectation of being able to sell it at a higher price later on.

It's also challenging to work out exactly how much steel is being consumed in China, although the industry associations forecast is for around 890 million tonnes of domestic demand for 2020.

Given that output is on track to exceed 1 billion tonnes for the first time, this may leave quite a gap between output and demand for the year as a whole.

Exports are unlikely to close that gap much, with steel product exports dropping 17.6% to 32.9 million tonnes in the first seven months of 2020 compared to the same period a year earlier.

It appears that the iron ore and steel sectors are placing a rather large bet that Beijing’s efforts to stimulate the economy post-coronavirus will result in significant boosts to the main drivers of steel consumption, namely construction and infrastructure.

There is some evidence of this, with property investment picking up, growing 3.4% in the January to July period, compared with the same period last year. This may sound modest, but it’s worth noting that in the January to March period, property investment was down 7.7% year-on-year, as China enforced lockdowns.

However, fixed-asset investment was down 1.6% in the first seven months of the year, although there was growth in steel intensive sectors like rail, which rose 5.7%.

But the question remains as to whether China can absorb all the steel it is producing, especially given that the rest of the world is unlikely to be much help with buying steel products, or manufactured goods made with steel.

Source:Reuters

The opinions expressed herein are the author's and not necessarily those of The Xinde Marine News.

Please Contact Us at:

media@xindemarine.com

.gif)

PIL launches Academy to strengthen workforce compet

PIL launches Academy to strengthen workforce compet  Coal shipments to advanced economies down 17% so fa

Coal shipments to advanced economies down 17% so fa  China futures market updates at close (Nov 14)

China futures market updates at close (Nov 14)  CISA: China's daily crude steel output down 5.7% in

CISA: China's daily crude steel output down 5.7% in  China futures market updates at close (Oct 31)

China futures market updates at close (Oct 31)  CISA: China's daily crude steel output down 1.2% in

CISA: China's daily crude steel output down 1.2% in