Capacity growth on the Asia/Europe maritime routes are set for substantial increases in 2019 and 2020, with vessels aggregating nearly 1.1 million twenty-foot equivalent units (TEUs) set to be delivered in the period, following an increase of 530,000 TEU capacity delivered in 2018.

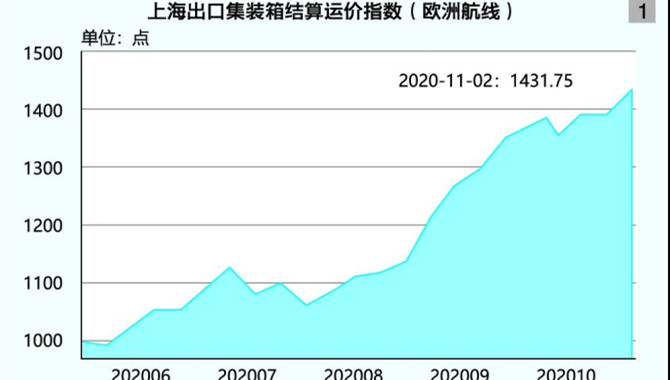

As a result of this extra capacity, freight rates on Asia/Europe routes are expected to come under increasing pressure, but even so Drewry shipping consultants estimates that rates could increase by an average 6.5 percent this year compared to 2018 rates (which were 25 percent lower than 2013 levels).

Attempts to mitigate the effects of these behemoths entering the trades includes deploying ultra-large container ships (ULCS) on the Asia to Middle East trades for the first time, slowing vessels down and adding an extra ship to a number of services and increasing the number of blank sailings.

Vessels Value, a London-based shipbroker and shipping data specialist, indicated that there are 90 ships of more than 18,000 TEU currently on order and slated for delivery this year and next. These vessels can only be deployed on the Asia/Europe trades due to their size and will add significant capacity to the 120 ships aggregating 1.8 million TEU already in operation on these routes.

Simon Heaney, Senior Manager of Container Research at Drewry, told FreightWaves that ULCS with an aggregate capacity of 450,000 TEU are due for delivery this year and are set to be deployed on trades operating between Asia and Europe.

Most of these vessels will be delivered to the Ocean and 2M alliances. Chinese operator COSCO, part of the Ocean Alliance, will take delivery this year of six vessels of between 19,000 and 21,000 TEU; while MSC, of the 2M alliance, has ordered 12 vessels of 23,000 TEU with an estimated seven or eight of these being delivered in 2019, according to Daniel Richards, an analyst at Maritime Strategies International (MSI).

Richards believes that MSC is eager to receive as many of these vessels as possible because they will be fitted with scrubbers and will be able to use cheaper high-sulfur fuel after the new regulation on the use of high-sulfur fuels is enforced on 1 January 2020 (IMO 2020). After this date vessels not fitted with scrubbers will need to use the substantially higher-cost low sulfur fuel.

IMO 2020 will lead to increases in the cost of fuel for most ships, and extra shipping capacity will also be available (putting pressure on freight rates). Therefore, vessel operators will attempt to mitigate the worst effects of these negative factors by increasing the number of blank sailings (in which a ship misses a week in its schedule), by increasing the number of ships in a particular service, and by slowing all those ships down, thereby reducing fuel consumption.

The overcapacity in the trades was exacerbated last year with some 530,000 TEU in ULCS delivered. Although Heaney expects that some 10 percent of ships on order for delivery this year may not in fact arrive until next year, this will only prolong overcapacity issues, as next year a further 620,000 TEU in ULCS capacity is again due for delivery.

Heaney admitted that the Asia/Europe trades were “already over-supplied,” and that the market will continue to be “challenging” for operators. However, Heaney believes container ship operators are “adept at managing the process [of deploying ULCS] cascading smaller ships in smaller trades.”

In addition, Heaney said that for the first time, the Asia to Middle East trades are about to see 20,000 TEU vessels deployed into this region.

“Ocean Alliance’s ‘Day 3’ network revamp will include hiving off the Far-East-Middle East leg from a Transpacific pendulum service to create a dedicated Far East – Middle East service, the ME5. The new dedicated loop is expected to use 20,000 TEU units instead of 10-13,000 TEU ships on the previous loop.” A pendulum service is so-called because it straddles two trades, in this case starting on the U.S. West Coast across the Pacific and then heading to Europe via Asia.

The effect of the new capacity arriving, on what is an already over-tonnaged trade, is persistent pressure on freight rates. However, with some growth in the trades and mitigating action, the pressure will progressively ease.

Heaney said that the expected rate increase of 6.5 percent in 2019 comes on what is a “very low base,” with freight rates 25 percent lower than 2013. Perhaps coincidentally, this was the same year that the first 18,000 TEU ULCS vessels were deployed by Maersk.

Drewry also points out that to achieve the rate increases ships must have a greater utilization rate of 90 percent (90 percent of capacity of the ship must loaded). However, westbound Asia/Europe utilization has averaged about 80-85 percent; should that level of utilization persist then rates will again slip.

Meanwhile, Richards at MSI also noted that the Ocean Alliance will not add any capacity to the Transpacific trades because of concerns over a trade war. And with the over-capacity pressures in the other major trade from Asia to Europe, it will add pressure to other trades.

“It will increase the pressure on freight rates in services from and to South America and services to the Indian subcontinent, which will receive more capacity. North/South rates will be under pressure, and that means that 2019 will be a very challenging year,” said Richards.

Source:Drewry

Please Contact Us at:

admin@xindemarine.com

.gif)